Future-you needs this

Retirement may feel like a lifetime away. But, time flies. Milestones come and go. And the truth is, without a robust and tailored retirement plan in place, you could easily find yourself living out your later years in stress, money panic and a tonne of regret.

A happy retirement is a financially secure one; it’s as simple as that. By putting the plans into place now - and slowly but surely building your investments - you can sleep easy in the knowledge that everything you’ve ever wanted is waiting for you.

So, you’re ready to think about your retirement?

Excellent - that’s music to our ears! The great news is that you don’t have to tackle this road on your own. We’re here to help you build a retirement plan based on your current lifestyle and commitments and your dreams for the future.

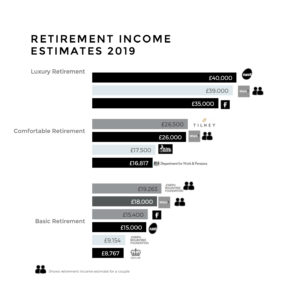

HOW MUCH DO YOU NEED TO RETIRE?

This is one of the most common questions our customers ask; the truth is, there is no clean cut answer! We’ll work with you to identify how much you personally need to invest in order to have a retirement that fulfils all your aspirations, based on your appetite for risk and capacity for investment.

BUILD FOR YOUR FUTURE

Haven’t reviewed your pension in a while? It’s time you did! We’ll identify how much you will need throughout your retirement, how much you need to save every month, ways to boost your retirement fund and any tax-efficient pension and savings plans that could maximise your money.

TRACK YOUR PROGRESS

It’s important to know where you’re at in your retirement saving journey; you can check in on this 24-7 with our exclusive digital investment platform. Wherever you are in the world, your financial planning will be right at your fingertips.

Learn more about our award winning platform

PENSION CONSOLIDATION

It’s common to have countless pension pots floating around - but chances are, you’d rather have all of your investments in one place. We can review your current fees, benefits and fund performance and if appropriate help you consolidate your pensions.

PENSION 01 FACTS

“Those who receive Financial Advice are on average 9.7% more likely to save and 10.8% more likely to invest for their retirement.” -

International Longevity Centre-UK (ILC-UK)

Get Retirement Ready.

Discover everything you need to know about planning your retirement in our expert guide

RETIREMENT PLANNING ADVICE

There’s never been a better time to plan, save and invest.

Reviewing your retirement arrangements is always a good idea. Whether you think it’s too far away to worry about or you’re scared you’ve left it too late…

Now is the right time to take back control of your future wealth.

Because retirement? It’s exciting. It’s your opportunity to step into the version of you that you’ve always wanted to be.

So, why wait? Give your future-self the gift of financial freedom.

Don't miss

Our most popular posts

These are some of our most popular posts. Click below or head over to our blog to see other helpful articles on pensions, retirement and investing.

Arrange a virtual coffee with an expert

No fees, no commitment, no hard sales, just a quick chat with one of our experts to see if we can help

Frequently Asked Questions

Retirement planning doesn't have to be complicated, with the right plan in place, and the right support, your dream retirement can feel like a breeze.

We've laid out some simple steps in retirement planning below, but if you get stuck, just reach out and one of our retirement planning specialists will be happy to help you:

- Decide what type of retirement you want to enjoy

- Set a retirement date

- Work out a retirement budget based on what feels like a good retirement income for you.

- Request a pension forecast - request your state pension forecast here https://www.gov.uk/check-state-pension

- Get your pension estimates - track down old pensions with the Pension Tracing Service (0800 731 0193)

- Talk to a Financial Advisor to create a retirement plan, work out how you will pay down any debt and if it's worth consolidating any old pensions

- Put your retirement plan in action and look forward to enjoying your retirement.

- Don't forget to periodically review your plans every year to make sure you're on track, because circumstances can change and the earlier you respond the more time you have to course correct.

Client Testimonial

Vicky Martin

"He communicates clearly, is reliable and trustworthy"

I’ve received financial advice from Simon for over 10 years and would be happy to recommend him. He communicates clearly, is reliable and trustworthy – a pleasure to work with!

Why put off until tomorrow what you can do today?

Take the first step