Over £80million has been transferred out of Final Salary pension schemes since the biggest changes to pension rules for a decade were brought into force in the UK in 2015. And although 2020 and 2021 have seen fewer people opting to cash in their final salary pension than the highs of 2018, there are still plenty of people wondering if final salary pensions can be cashed in.

Transferring your Final Salary pension is not a decision to be taken lightly. For one it’s a decision that’s irrevocable. It’s a high-risk area with high stakes for most people i.e. the security of their financial future, so it’s imperative that whatever decision you make is the right one for you.

As part of our dedication to ensuring people have access to high quality, balanced information from a qualified specialist, we’ve put together 11 factors you should consider before you transfer your final salary pension…

- Your Transfer Goals

- High Transfer Values

- Timing of Transfer

- Flexibility

- Early Retirement

- Tax-Free Cash

- Death Benefits and Inheritance

- Health

- Scheme Solvency

- Investment Risk

- Lifetime Allowance

1) What are your Transfer Goals?

As Simon Sinek advised in his bestselling book ‘Start with Why’ – understanding what is driving you is a great place to start any endeavour. It is so important to consider why you want to move your pension and to understand what your goals are before you transfer.

Often when we talk to customers we look at alternative paths that could help them meet their goals without having to transfer their pension. Sometimes there is a win/win situation to be had, other times there will be trade-offs involved – it is highly unlikely you’ll be able to replicate the exact benefits of your Final Salary Pension when you transfer out.

Understanding your goals will help you to make a more informed decision when deciding whether or not to transfer your pension. You’ll be able to weigh up the relative value of reaching your goal versus the costs and or risks of transferring your pension.

Examples of the types of goals we often see are:

- Early Retirement

- Access part of my pension from 55 to fund an early semi-retirement (i.e. work part-time)

- Use my tax-free lump sum to pay the mortgage off early or to clear debts

- Use a personal pension as a tax-efficient way to pass money on to my children and loved ones when I die

- Use my tax-free lump sum to fund the purchase of an investment property or a retirement property abroad

- Use my tax-free lump sum for home improvements

- Use the tax-free lump sum to pay for holiday plans or to buy a motorhome

2) High Transfer Values

The amount you are offered when you transfer your pension is known as your final salary pension Cash Equivalent Transfer Value. It should be a fair representation of the value of the benefits you are giving up. Transfer values have been at record highs for the last few years but they shouldn’t be the tail wagging the dog. A high transfer value on its own isn’t a good enough reason to leave a generous Defined Benefit Pension Scheme.

It’s important to note that your Pension Scheme Administrator decides how much you get based on the rules set by the scheme. So the fact that on average, transfer values are high at the moment, doesn’t necessarily mean that your transfer value will be higher.

The factors they use to decide how much you’ll get from a final salary pension cash in or transfer often include:

- Age

- Scheme retirement age

- Scheme funding position

- The performance of the scheme’s investments

- Cost of living and inflation rates

- Life expectancy of the ‘average’ scheme member

- Whether you are married or single

- The financial health of the pension scheme itself

- The number of people transferring out of the scheme

How investment performance has affected pension transfer values

Pension Schemes “discount” transfer offers by the return they expect to make on their investments: the lower the return, the higher the sum needed to pay the pension and hence the higher the transfer value.

Many Final Salary Schemes have switched to low-risk Gilt Bond investments to ensure that they can pay their member’s pensions. The historically low-interest rates that the UK has seen in recent years has affected the returns of these Gilt bonds – known as gilt yields, which has pushed up the value of pension transfers.

![]()

Fluctuating transfer values

It is important to know that Pension Scheme trustees have the right to adjust transfer values so they represent “fair value” and do not adversely affect other members. So do not assume that your transfer value will be the same as your colleagues – if the schemes funding position changes or lots of people transfer out in a short space of time, they can change the rules and your transfer value can fall.

Your final salary pension Cash Equivalent Transfer Value is calculated by your Scheme Trustees on the basis of a typical member of the scheme. If you do not fit the mould of your scheme’s ‘typical’ member this could either work in your favour or feel unfair as you’ll see later, when we cover Health.

Interested to know what your CETV could be? Why not try our Final Salary Transfer calculator?

3) Timing of Transfer

Knowing when is the best time to transfer your pension is a tricky one, but it is still something you’ll need to consider. Unfortunately, there is no crystal ball that will tell you this.

We see people struggle to decide as they try and work out whether market influences will increase their Transfer Value over time and they wonder “ Will I get more if I wait?”. Put simply, there is no way of knowing for certain whether values may rise or fall in the future.

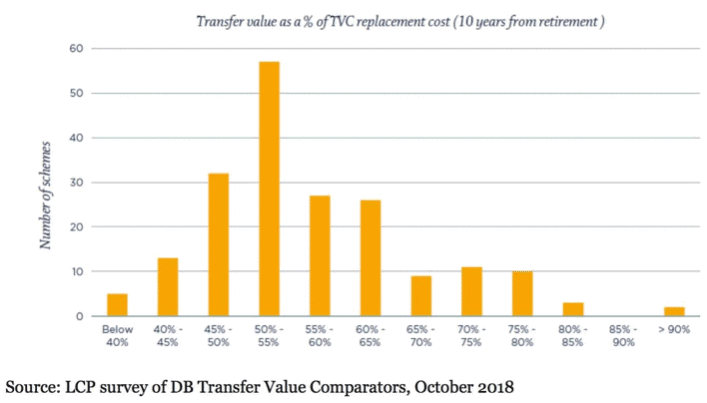

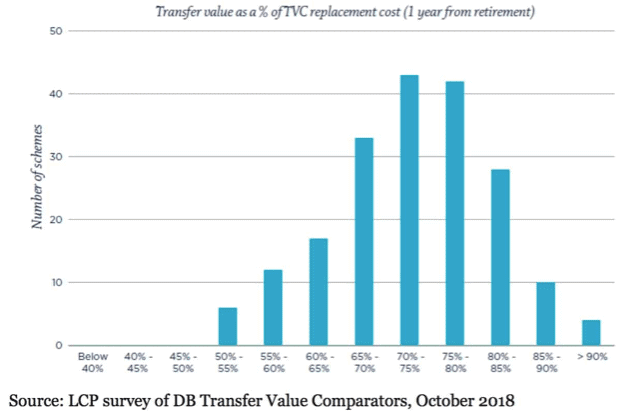

Research published by Royal London and LCP has shown that the relative value of transfer values tend to rise the closer people are to retirement.

The graphs below show that on average those that are 10 years away from retirement are more likely to have transfer values with a lower comparative value in a defined contribution arrangement than those that are closer to retirement.

So you’re likely to be offered more the closer you are to retirement. However, with other factors affecting how transfer values are calculated, this certainly isn’t a guarantee as external factors could also negatively influence the amount you are offered.

From our experience, as pension transfer specialists we’ve seen people miss CETV deadlines to see 6-figure reductions in the value of their pension, conversely, we’ve also seen people defer a pension transfer only to see their transfer value rise by 6-figures – obviously, they had a sizeable CETV to start with but there’s no standard when it comes to defined benefit transfer values.

Understanding the True Value of your pension

Advisors must now use a Transfer Value Comparator (TVC) that shows the value of the benefits being given up and the cost of purchasing the same income in a Defined Contribution (DC) pension arrangement. This replaces the old TVAS report.

The Transfer Value comparator aims to give you a better idea of the true value of the benefits you are giving up.

What we advise

Don’t rush! It is far more important that you make an informed decision that you feel comfortable with than making a rushed decision that you might regret later. Take your time to decide and get the best advice you can. Because, once it’s done, you can’t go back.

Considering a transfer? Arrange your free introductory call with a qualified Pension Transfer Specialist today. Call us now to schedule 02380 981161

4) Flexibility

Another thing to consider before you transfer your final salary pension is how flexible you need your money to be.

Final salary pensions are guaranteed, inflation-proof and often generous but what they aren’t is very flexible.

If flexibility is something that’s important to you, it might be beneficial to consider a transfer to a more flexible defined contribution pension arrangement:

Pension flexibility for Tax-planning

With a final salary pension, you will receive a guaranteed amount paid to you on a monthly basis once you hit your scheme’s pensionable age (unless you opt to defer). If you opt to carry on working and still receive your pension your personal tax liability could increase, in some cases substantially if you’re a higher rate taxpayer.

If you have a defined contribution pension you can opt to go into ‘flexible drawdown’ which allows you to flexibly access your tax-free cash as well as your pension pot through retirement. By doing this you can manage your income tax-efficiently by reducing the amount you take out of your pension whilst you’re still working.

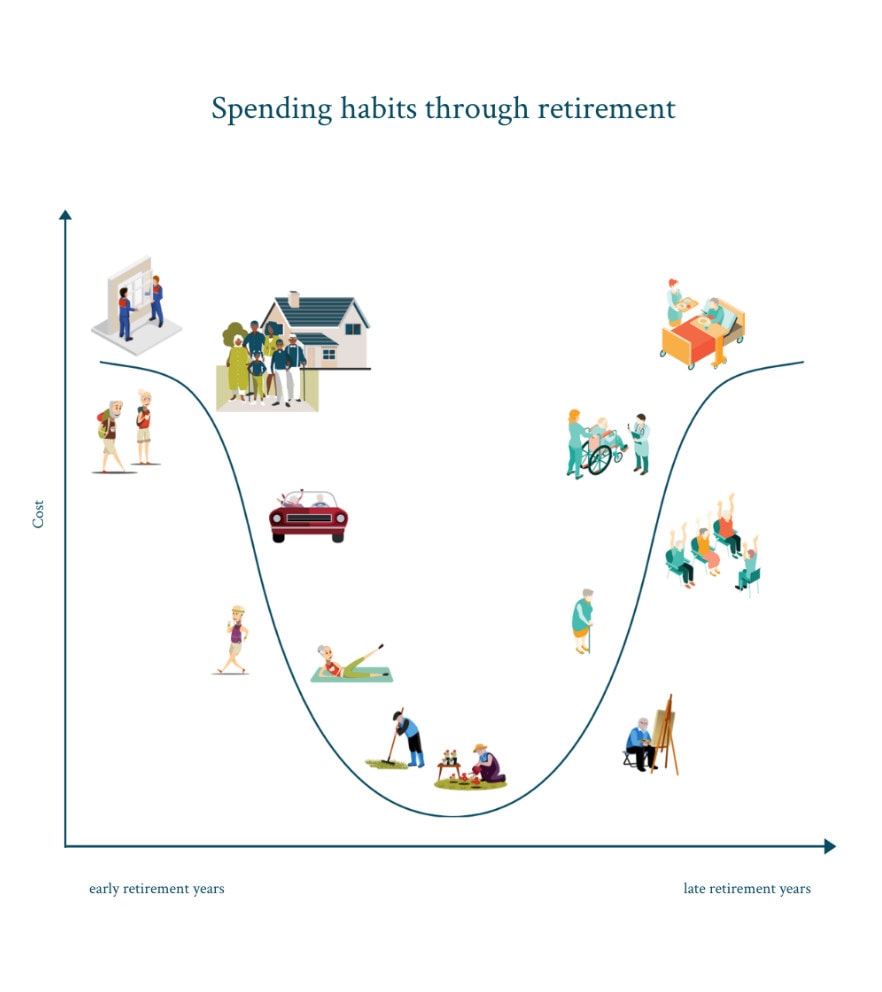

Pension Flexibility for Lifestyle

The cost of retirement tends to change over time. In earlier retirement individuals tend to spend more on big holidays, home improvements, new cars and helping children through university or on the property ladder. In mid-retirement people tend to be more settled, choosing to spend more time at home and less time travelling. For 1 in 3 retirees, late retirement can bring with it the need for care.

With a fixed income, you might struggle to adapt to changing lifestyle requirements. A more flexible approach to income as you find with flexi-access drawdown may suit your needs better.

Is this your only pension? If you have multiple final salary pensions you may opt to transfer one to give you some flexibility whilst retaining other guaranteed pension benefits.

Consider whether you actually need the flexibility that a transfer would offer you, is there an alternative course of action or are you better off with less flexibility and safeguarded income?

5) Early Retirement

Early retirement is often cited as one of the main reasons where someone is considering a final salary pension transfer. Whilst most schemes do allow for early retirement there are a few factors to consider if this is a priority for you:

- You’ll need your pension scheme administrator’s permission to retire early

- Your pensionable income could be reduced significantly.

- Personal pensions can be accessed from 55 without penalty

Your pension scheme administrator decides the calculation used to work out how much you’ll get if you decide to retire early. In less generous schemes you may have to give up a significant amount of your pension in order to retire early. If this is the case then you’ll need to consider whether you could be better off transferring your pension into a defined contribution arrangement where you won’t be penalised for accessing your pension from the age of 55.

6) Tax-free cash

The new pension rules introduced in 2014 allowed people to access 25% of their pension tax-free at 55. However, how this works for final salary pension schemes vs defined contribution schemes is very different.

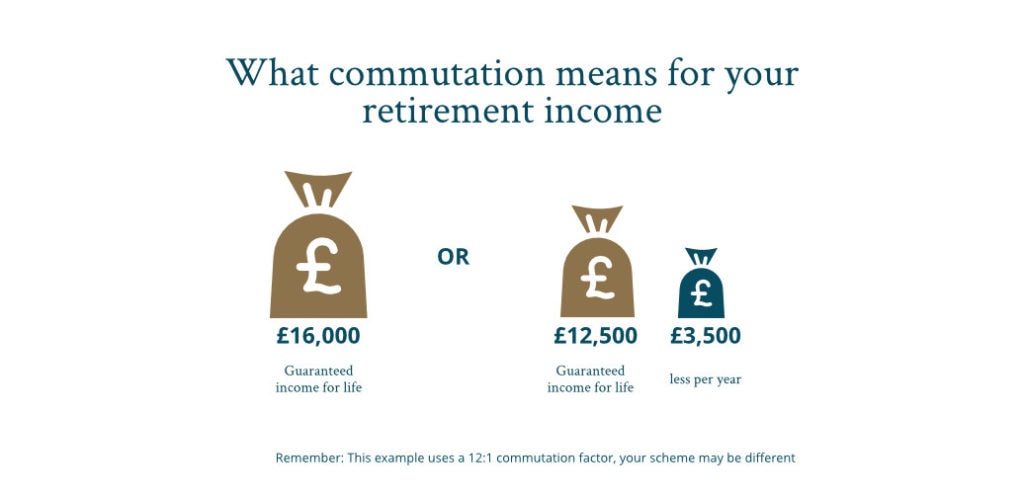

With a Final Salary Pension Scheme, your tax-free cash is usually offered as a Lump sum often at retirement age. In most Final Salary schemes you give up some of your income in return for tax-free cash lump sum. This is known as “Commutation”. The commutation factor can vary from scheme to scheme, so some may be more generous than others.

Because of the way this tax-free cash is calculated by your pension trustees, it’s often possible to access a larger amount of tax-free cash by transferring to a personal pension.

If you do transfer, you don’t have to take all of your tax-free cash as a lump sum, you can opt to take smaller lump sums over time or use the cash as income. Either way, the first 25% is always tax-free and once you go over that you’ll pay tax at your marginal rate.

Considering a transfer? Arrange your free introductory call with a qualified Pension Transfer Specialist today. Call us now to schedule 02380 981161

7) Death benefits and Inheritance

From 6 April 2015 major changes to Pension Death Benefits took effect when the pension ‘death tax’ was abolished. Since 6 April 2015, it is the age of the person who dies that affects the tax treatment of the benefits and the restriction that income can only be paid to a ‘dependant’ has been removed, which affects both drawdown pensions and annuities.

Pensions sit outside your estate and as such are not liable for Inheritance tax. For this reason, they are a useful way of leaving a legacy whilst reducing your inheritance tax liabilities.

Defined Benefit pensions and defined contribution pensions are not subject to the same rules when you die. Defined Contribution pensions can be passed on to any named beneficiary on death. Final salary pensions are treated differently when you die.

Death Benefits and Drawdown Pensions

If you die before age 75 your pension can be paid as a lump sum or as a drawdown pension to any named beneficiary tax-free, irrespective of whether you have started taking money out of your pension or not

If you die after age 75 your pension can be paid as a lump sum or as a drawdown but it will be taxed at the beneficiary’s marginal rate.

Read more: What happens to your defined contribution pension when you die?

Death Benefits and Final Salary Pensions

The above rules do not apply to Final Salary Scheme pensions. This means that the payment of a dependants’ pension from a defined benefit scheme will be taxed at the dependant’s marginal rate, regardless of the age of the individual when they died.

Inheritance rules for a Final Salary Pension differ from scheme to scheme, but as a general rule your scheme will usually provide a reduced survivors pension to your spouse or partner that is guaranteed for their lifetime and protected against inflation. The amount paid is normally 50% of your pensionable income but we have seen some pensions offer as little as 20% of the initial benefit

Survivors pensions will normally only be paid to a spouse or a dependent child up to the age of 23. It is not normally possible to nominate any beneficiary as is the case with a drawdown pension or lifetime annuity.

Read more: What happens to your Final Salary Pension when you die.

8) Health

If you suffer ill health and your life expectancy is severely limited, your final salary pension doesn’t offer much flexibility. Whilst you may be able to opt for early retirement, you will still be offered a reduced amount for doing so and any survivors pension will be based on that reduced amount.

If you opt to transfer your pension to a drawdown pension you can flexibly access your pension pot opting to take as much or as little as you need and you have the option to leave any remaining money free of inheritance tax to any beneficiary you name.

9) Scheme Solvency

We have seen many high profile pension scheme collapses in recent years including British Steel, BHS and construction giant Carillion and it has been highly publicised that many Final Salary Pension Schemes were underfunded and at risk of future collapse. Since 2016 steps have been taken by these schemes and the businesses running them to reduce the deficit but many remain underfunded and in need of more work.

For anyone worried about the solvency and future of their scheme, the Pension Protection Fund (PPF) acts as an insurance policy should your employer’s Final Salary pension scheme get into trouble or if the business goes bust in the future. The fund currently protects 90% of the value of members pensions.

Payouts also rise in line with inflation each year, subject to a cap. So unless you have built up a very large pension you are unlikely to be affected.

If you have already started drawing your pension then the PPF guarantees 100% of your pensionable income.

10) Investment Risk

You can’t consider a defined benefit pension transfer without considering the investment risk you’ll be taking on when you move to a defined contribution pension. Once your money has been transferred out you’ll be opening yourself up to inevitable risks associated with investing.

Final Salary pensions offer a guaranteed income for life, protected against inflation. The scheme trustees bear the risk of their investment choices, even if their investments do badly you still get the same amount. If you move your pension to a drawdown arrangement, the most popular choice for those transferring, you take on the risk.

The main risks you’ll face are:

- Investment Risk – if your investments don’t perform as well as hoped then you could have less money in retirement.

- Withdrawal Risk – If you don’t plan adequately and you take too much too early in retirement you may deplete your pension pot and run out of money.

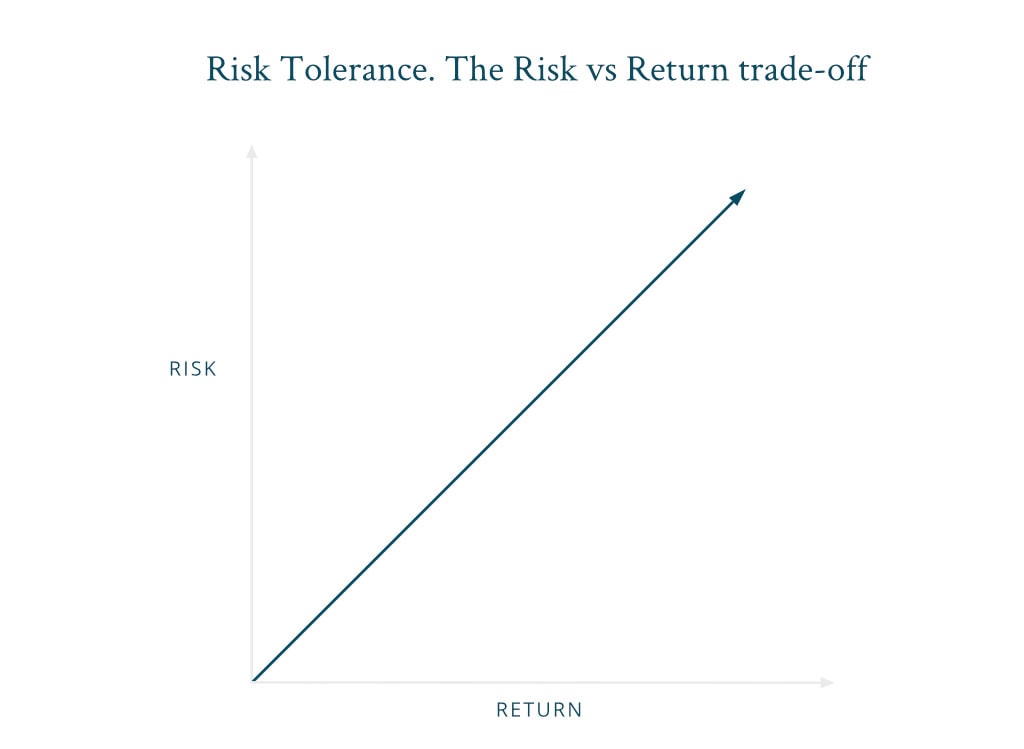

Ask yourself: How much risk are you comfortable with?

Risk and investment return are positively correlated, that is, the higher the level of risk, the greater the potential for returns and losses.

It is important to understand how comfortable you are with risk and how much risk you could tolerate. Your Risk Profile or tolerance will be linked to your goals but also your deeply entrenched views and emotions concerning money. Often partners can have completely different views on risk and you’ll need to make a plan for your money that you are both happy with.

There is no way to eliminate risk completely – even cash, which most people assume is the safest investment, is at risk of inflation.

Why does my risk profile matter?

Your attitude towards risk and your ability to absorb losses will affect how your money should be invested and could impact on whether you can meet your goals. You should ask yourself “How much money do I need from my pension every year?” and ask your financial adviser “If my money is invested according to my risk profile, how likely is it that I will be able to meet my retirement goals – and for how long?”

High Risk = higher chance of returns or loss, Low risk = lower chance of returns or loss.

Risk vs Return – how do you feel about it?

Here is an example scenario from our risk questionnaire – you’ll be asked to look at examples of potential losses versus potential gains over a given time period and asked to pick which scenario you would feel most comfortable with.

Investing goals

There are two principal parts to investing: Investing for Growth and Investing for Income. Depending on your goals, you may lean more towards one than the other or try and combine elements of both. Both involve long-term investment strategies.

Investing for Growth

i.e. I don’t need the money in my pension, I want to leave it as a legacy for my children. Your money would be invested with the sole goal of growing the amount you have. Where you have income producing assets such as dividend payments or fixed interest payments from bonds, these would be reinvested to help boost the value of your pension/investment.

Investing for Income

i.e. I plan to take regular amounts from my pension in order to fund my retirement. Whilst the investment strategy may be similar to above, investing for income allows you to make regular or ad hoc withdrawals from your pension. You can either use the capital from your pension, money from dividend payments, fixed interest payments or a combination of all three to do this.

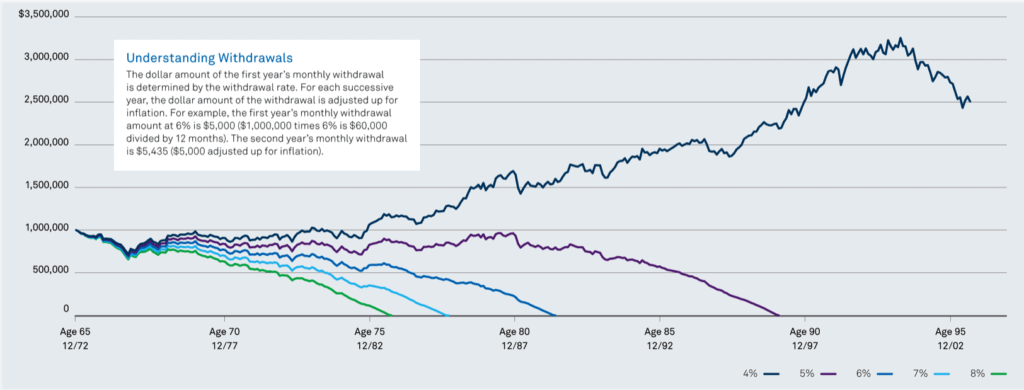

Safe Withdrawal rate

When investing for income it’s important that you withdraw a sustainable amount from your pension, you don’t want to take too much and end up running out of money too soon. Unlike a Final Salary Pension that provides a guaranteed income for life, a drawdown pension comes with the responsibility of managing your money. Once it’s gone, it’s gone.

11) Lifetime Allowance Limits

The Lifetime Allowance (LTA) is a limit on the value of payouts from your pension schemes that can be made without triggering an extra tax charge. It was reduced from £1.25m in April 2016 and now stands at £1,073,100. It is due to increase in line with inflation (CPI) each year.

The rate of tax you pay on pension savings above your lifetime allowance depends on how the money is paid to you:

- If you take your money as a lump sum you’ll pay 55%

- If you take your money as pension payments or cash withdrawals you’ll pay 25%

This is on top of any tax payable on the income in the usual way. See examples here

The way LTA is calculated versus the calculation for transfer value for Final Salary Pensions means that you could go over the LTA if you transfer, even if you would have been under the threshold within the scheme.

Lifetime allowance is calculated by your pension provider and is usually worked out on 20 times your first year’s pension plus your lump sum. This means someone with a £50,000-a-year pension income would still fall within the new £1,073,100. limit and could avoid the tax. If you do exceed the LTA, your Pension Scheme Administrator will deduct the additional 25% tax at source from your pensionable income, they’ll adjust the amount as soon as your pension becomes payable.

Deferring Lifetime Allowance Tax

If you’re already over the LTA in your Final Salary Scheme then the flexibility of a transfer may work in your favour. Under defined contribution arrangements, current tax rules allow those using Flexible Drawdown to defer the Lifetime Allowance Tax (LTA) until they are 75. As long as you keep your withdrawals within the LTA limits up to age 75 you’ll gain the benefit of a largely tax-exempt investment account until that date, you can put off paying the LTA tax until your 75th birthday. You’ll pay the surcharge tax on the excess value of your pension pot.

Estate Planning – LTA vs Inheritance tax

If you have no need for the funds in excess of the LTA then you could consider leaving these invested in your pension pot. Although you have to pay the LTA charge of 25% at age 75, any money in your pension sits outside of your estate and therefore not liable for Inheritance Tax.

If you die after your 75th birthday your ultimate beneficiaries will have to pay income tax on the benefits but this may be preferable to you paying income tax on the income and inheritance tax (currently 40%) on any funds that remain in your estate.

So you can see, there’s a lot to consider and a lot of different factors that could affect your decision to transfer. If you do have any questions feel free to drop us an email at [email protected], we’ll get our pension specialist to reply.

{kind=link}