Members of the BT Defined Benefit Pension Scheme have seen a number of changes over recent years and months. With a growing number of questions being asked, our Pension Specialist Simon Garber seeks to provide some answers for members of this Final Salary Pension.

Why has my BT Pension Transfer Value gone up?

We have seen an increase in enquiries from those with a BT Defined Benefit Pension Scheme wanting to understand why there has been a increase to their Cash Equivalent Transfer Value in recent months.

We have previously looked at what causes High Pension Transfer values in general and it remains true that there can be a number of factors at play when it comes to increasing transfer values. Some are market factors and some are at the discretion of your Pension Trustees, and it’s important to know that the factors that make up your Cash Equivalent Transfer Value (CETV) are subject to change.

In 2016 members of Defined Benefit pension schemes across the UK reported rising transfer values, which was linked to low Gilt Yields pushing up transfer values, however over the last year or so, Gilt Yields have been rising and many people have seen their transfer values fall.

This is where BT have bucked the trend. Members of the BT Defined Benefit Pension Scheme have reported rising pension transfer values over the last few months and it seems it is linked to changes made by the Pension Shceme Trustees.

Whilst Pension Scheme Trustees rarely publish details of all the factors they use to calculate DB pension transfer values, it has been reported that The BT pension scheme has made changes to the factors it uses to calculate your pension value for early retirement.

This favourable change in Actuarial Reduction Factors may mean that any transfer value you receive now might be higherthan you have previously received, with some scheme members reporting that their transfer value had increased from 21 times their annual pension to 28 times their annual pension.

What’s my Transfer Value?

A Cash Equivalent Transfer Value (CETV) is the amount your pension scheme will give you if you decide to transfer your pension. It is supposed to represent the value of the benefits you are giving up. If you don’t have yours yet you can use our simple calculator to get an estimate.

Early Retirement and Transfer Value – What’s the link?

A Cash Equivalent Transfer Value is supposed to be a fair reflection of the market value of your pension. If more favourable terms are given to Early Retirement i.e. you get more money per year, then the cost of your pension to the Pension Trustees effectively goes up and the CETV needs to go up accordingly to reflect this.

Defined Benefit Pension Schemes and Protected Early Retirement

Before you consider a transfer, it is worth checking whether you have a guaranteed early retirement age. Some members of the BT Defined Benefit pension scheme can access their DB pension from 51. It is important to note that if you transfer out, the earliest you will be able to draw from a private pension is 55.

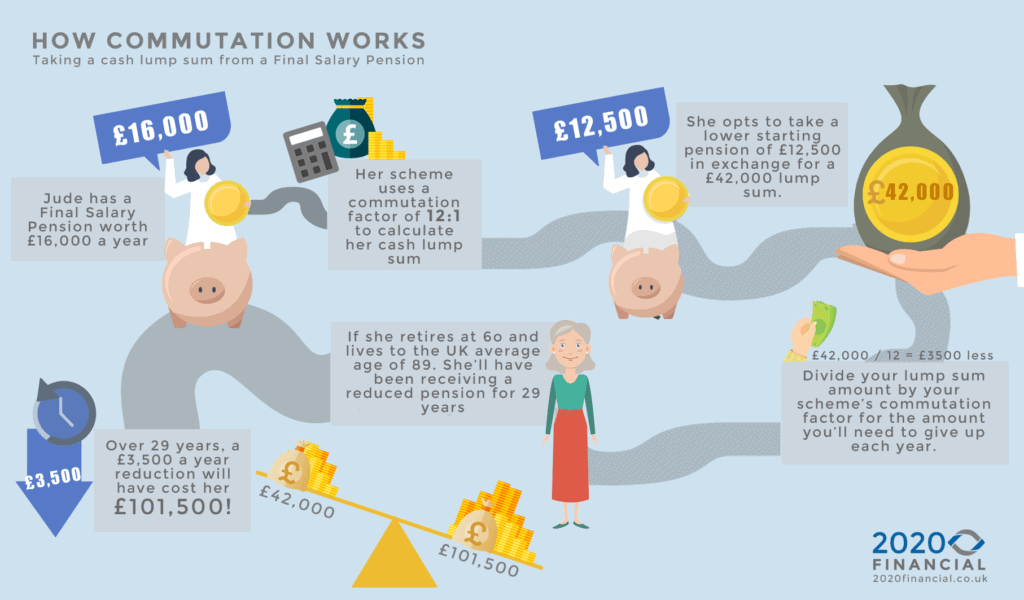

Understanding the cost of early retirement

The change to commutation factors means you’ll get more than you previously would have done if you take early retirement. It is worth remembering that the guaranteed amount you receive will still be reduced for every year that you take your pension below the normal retirement age for your scheme.

If you’re still working and you opt to take your pension early you should also be aware of the income-tax implications of this. If your pension is going to take you into a higher-rate tax bracket then it may be in your interests to delay taking your pension until you plan to retire to reduce the amount of income tax you’ll be paying.

Don’t forget your Tax-Free Cash

The amount of tax-free cash you are entitled to will also reduce if you opt for early retirement (and this could be significant) so it’s worth requesting an estimate from your Pension Trustees to work out if it’s actually worth taking your retirement early.

Can I access my cash before 55 if I transfer out of the Scheme?

In a word, no. If you transfer your Defined Benefit pension, you’ll need to find a suitable Defined Contribution pension for it to be transferred to – more than likely this will go into a SIPP (Self-invested Personal Pension). Regardless of what type of Defined Contribution pension you choose, you won’t be able to access it until you are 55, apart from rare cases where severe ill-health can be demonstrated.

Do not get lured into false claims that you will be able to access your pension before you are 55. – Pension liberation, as it is known, is a scam and you could end up with a huge tax bill and no pension pot!

But I’ve heard about a Buddy Transfer – what is this?

We’ve had a few questions about “Buddy Transfers” as a way of protecting tax-free cash and protected early retirement age whilst transferring out of your scheme. What people are referring to is known as a Block Transfer* which is a transfer of two or more people at the same time from one pension scheme to a new pension scheme.

Whilst it may be possible to protect your guaranteed tax-free cash and early retirement age through a block transfer, it is important to know that a Defined Benefit Pension Transfer may not be in your best interests, even if you and a colleague have similar transfer offers. What may be right for one person, may be completely inappropriate for another and it’s really important not to get drawn into the herd mentality when it comes to your financial security. Each transfer must be considered under its own merits and based on each person’s own circumstances.

*Block transfer conditions: A transfer is a block transfer if it involves the transfer in a single transaction of all the sums and assets representing accrued rights under the scheme from which the transfer is made which relates to the member and at least one other member of that pension scheme. Before the transfer, the member must not have already been a member of the registered pension scheme to which the transfer was made for longer than 12 months before the date of the transfer. The only exception to the 12 month eligibility period of scheme membership applies to members of personal pension schemes prior to 6 April 2006, where membership of the scheme was in respect of receipt of contracted-out rebate monies only.

Other Changes to the BT DB Pension Scheme…

In December 2018 BT lost an appeal to change the way it worked out pension increases paid to “section C” members of its defined benefit pension scheme. It had been seeking to switch from retail prices index (RPI) to the CPI Consumer price index, which is often lower.

Members of its final salary pension scheme enjoy a guaranteed annual income in retirement that rises in line with inflation each year. It was estimated that members stood to lose an estimated £24,000 each in future pension benefits.

BT argued that since the RPI is no longer widely used in government that its use for calculating pension increases was inappropriate and the lower CPI should be used. However, unions claimed that this would have transferred an estimated £2bn of wealth from scheme members to shareholders and the move was blocked by the appeal court after BT lost it’s original High court challenge in January 2018.

Download our Definitive Guide to Final Salary Pension Transfers today for more information about the risks and benefits of transfer.

The importance of getting financial advice

Time and time again we see people resorting to forums and social media for advice on their pension. This is an extremely complex area. Any decision concerning your Defined Benefit pension is one that could significantly impact you financially for the rest of your life and you should only be taking financial advice from a professional that is qualified to give it.

A Financial Adviser Will

- Help you understand all of your options

- Understand your goals and situation

- Talk you through any cost implications of your various options

- Advise on alternative actions that will help you meet your goal

If you’d like to talk to a pension transfer specialist about your BT Final Salary Pension, book a free introductory call today.

{kind=link}