You’re about to turn 55. On your right is a teetering tower of mortgage repayments, debt and “oh but can’t we just run away to the Maldives?”, and on the left is one heck of a pension pot. We’d hazard a guess that the question “can I cash in my drawdown pension?” is looming at the forefront of your mind?

Can I cash in my drawdown pension? In a word – yes. Current rules allow you to access your Drawdown pension in full from the age of 55 (57 from 6 April 2028). But, there are potential tax implications to consider, as well as the impact cashing in your drawdown pension could have on your financial future.

What may seem like an attractive choice could cost you dearly in the long run.

Choosing whether or not to cash in your drawdown pension is not an easy decision – it’s one that requires careful consideration and weighing up all the pros and cons. Luckily, that’s where we can help. Read on for our full guide on whether it’s possible for you to cash in a drawdown pension, and what aspects you need to be aware of if you’re considering cashing in your pension pot.

Should you cash in a drawdown pension?

Even if you can cash in your drawdown pension, that doesn’t necessarily mean that you should. As with most things, there are reasons for and against cashing in your drawdown pension.

If you are considering cashing in a drawdown pension, you should only do so as part of a well thought out plan, otherwise, you could end up damaging your long-term financial health (which could have a negative impact across all areas of your life), you could also end up with a large tax bill.

We cover how much you should drawdown from your pension in more depth in our article How much can I drawdown from my pension pot

The pros to cashing in a drawdown pension.

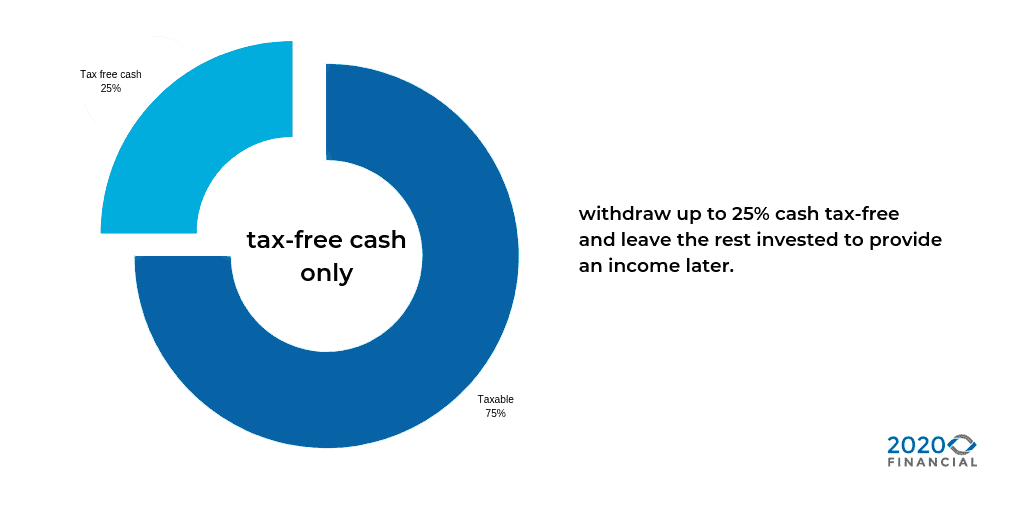

1. You can access up to 25% of your drawdown pension tax free.

When you cash in your drawdown pension, the first 25% can be taken tax-free. This can be done from the moment you hit 55 (57 from 6 April 2028), and is one way to take advantage of a tax-free cash chunk.

For anyone struggling with the ominous overhang of debt, it can be an attractive idea to wipe the slate clean. Afterall, you’re going to have considerably less income to pay it off once you enter your golden years. Plus, if you do stay within the 25% threshold, you can protect yourself from another bulky bill from the tax man.

2. You can take advantage of your 25% tax free sum across all of your pension pots.

If you have your fingers in lots of pension pot pies, it may be possible to cash in a 25% tax free amount across each pot.

Again, this can be enormously beneficial for those looking to clear out debt or a mortgage (and the interest rates and charges that come on top of it) so that you can start again and remove any unnecessary stress getting in the way of you living your best life.

However… While this quick fix may help you level out your current situation, it could damage your future one.

3. It can help you meet your lifestyle goals

We’ve seen clients access their tax-free cash from a drawdown pension to achieve all sorts of life goals, from buying a campervan to travel Europe in their retirement and buying a property abroad to helping kids get on the property ladder.

Having the flexibility to access cash from a pension can offer the freedom to achieve goals you might not have otherwise been able to afford.

The cons to cashing in a drawdown pension

1. Any money that you take out of your drawdown pension will be eligible for inheritance tax.

Pensions generally sit outside your estate for inheritance tax purposes.

The second you cash in your drawdown pension, it will be eligible for inheritance tax. That’s because once you take money out of your pension, it is considered part of your estate.

The thing about inheritance tax is it’s substantial; 40%, in fact. So, if you want to pass your pension onto a loved one, they could instantly lose 40% of the money that you put your time, work and energy into saving. Gone, just like that.

However, a pension pot protects your cash from inheritance tax. It’s the safest way to guarantee that your beneficiaries receive every single penny and that your hard-earned money isn’t taken away.

2. When you cash in your drawdown pension, it is no longer in a tax-efficient investment wrapper.

Similarly, when you take your investment out of a pension pot, it loses all of the tax-efficient benefits that it has been soaking up. Not only will it stop accumulating as much, but it will also start to drop… And pretty fast.

Why? Because if you take out over 25% of your drawdown pension, it will be taxed at your highest amount. The investment that you cash in will be added to your overall income: in the eyes of the taxman – once you pass £50,271 – this could very quickly see you move into the highest rate tax bracket.

In addition, if you plan to put your investment into your bank account, you will experience limited interest rates; especially in comparison to the benefits available with a pension investment. We explain this (and much more) in finer detail on our Pension Drawdown Advice page.

Essentially – without careful planning – you could find yourself on a hamster wheel of tax implications… Taxed for taking the money out in the first place, and then taxed on any money earned. And no one wants that.

TOP TIP: Take a look at the 5 best pension lump sum calculators to get a feel for the potential tax implications if you were to opt for a cash in.

3. You could meet your lifestyle goals, at a far greater cost

As humans, we can be pretty irrational about money. “We’ve seen people on incredibly low-interest-rate mortgages fixate about cashing in their pension to pay them off, even when they can more than afford the repayments and doing so will create a large tax bill”. Says Simon Garber, managing director of 2020 Financial.

If the cost to cash in a drawdown pension is greater than alternative actions, it doesn’t always make sense to do so.

4. You could run out of money.

Well, we had to save the biggest one for last, didn’t we?

Cashing in your drawdown pension could seriously hurt your financial future during retirement. It is crucial to have a clear and focused picture of how long your pension will survive (try our pension drawdown calculator here) once you have taken the lump sum out of it.

While you may have every intention of ‘refilling the pot’, do you have a strategic plan on how you will actually do that? Don’t forget that once you draw more than your 25% tax-free cash, you’ll trigger the Money Purchase Annual Allowance.

If you weren’t to reimburse the amount, how long would your pension last? Are you eligible for the full state pension (and can you realistically survive on that)?

You need to know the answers to these questions before making any decisions. We recommend that you speak to a financial specialist to map out some cash flow modelling and then seek independent pension drawdown advice from a retirement specialist.

TOP TIP: Use our Pension Drawdown Calculator to see how long your pension could last.

Cashing in a drawdown Pension: things to consider

If you have decided that a drawdown is the right choice for you, then there are a couple of things few steps that you will need to consider first.

1. You may not be eligible.

Not all pension schemes allow drawdown. If you have a defined benefit pension scheme, it isn’t possible and you will need to transfer out of the scheme. This is an incredibly specialist area, and one that you should discuss with a financial advisor before committing. This is something that we are experts in; we will not only provide impartial advice on whether this is the best choice for your circumstances and needs, but we will also orchestrate and manage the transfer process if you do wish to move forward.

Similarly, if you have an old defined contribution pension, you may also find that your scheme does not allow for drawdowns. Again, you will need to transfer out of the scheme. Although this is a far more straightforward process, it is vital that you check that you will not be leaving any benefits that you were unaware of: something that we are more than willing to help and support you with.

2. Can you manage your drawdowns sustainably?

If you are going to cash in your drawdown pension, then you need to be certain that you have a sustainable plan to manage your drawdowns.

Ideally, you will create this with an independent financial advisor who will be able to look at what you need, what you have and what will (or could be) coming in. They can feed this into a cash flow forecast which you can then give to an independent pension drawdown specialist.

How do I draw down from my pension?

If you have decided that a drawdown is the right choice for you, then there are a couple of things few steps that you will need to consider first.

1. Speak to your accountant

Nobody likes surprise tax bills, so we highly recommend speaking to your accountant BEFORE you withdraw any cash from your pension and check your tax liability. It’s not uncommon for the newly retired to be placed on emergency tax. You could end up paying more tax than you thought and you might not be able to claim a tax-rebate straight away.

2. Speak to your Financial Adviser

A financial adviser may be able to save you tax by helping you withdraw your pension in a more tax-efficient way. They’ll also be able to look at your finances as a whole and help to see if there’s a more effective way to achieve your financial and life goals.

3. Speak to your pension provider

If you’re in a Drawdown pension scheme you will need to contact your pension provider to request the withdrawal.

It usually takes between 2-3 weeks for drawdown requests to be processed so leave yourself plenty of time if you need the money by a specific date.

Get independent pension drawdown advice.

And that’s where we come in. Simon is a Pension Transfer and Retirement Specialist with over 15 years of experience. He is passionate about showing people that there is another way to do things, and that anyone can achieve financial freedom with the right guidance and support.

His advice is 100% impartial and based on a successful career delivering high-quality, person-centred, tailored financial advice that helps clients reach their financial goals.

Whether you are committed to cashing in your drawdown pension or are looking for honest advice on the best route for you, he’s here to help you; every step of the way.

{kind=link}