One of the questions we’re asked most often when we’re helping customers with their retirement planning is Can I take my pension at 55 and still work?

Under current rules, It is possible to take your pension at 55 and still work. If you have a defined contribution pension you could access part or all of your pension at 55 to fund a phased retirement or early semi-retirement but there are tax implications of doing this. In 2028, the age at which you can access your private pension rises to 57

If the idea of early retirement appeals to you, but you don’t quite have the retirement savings to fund a full early retirement, you might be looking for other solutions. The Pension freedoms announced in 2015 allow you to access your private pension pot from 55, which offers a whole world of flexibility in terms of retirement age and working in retirement. You might be surprised at the number of options that are available to you.

Can I take my pension at 55?

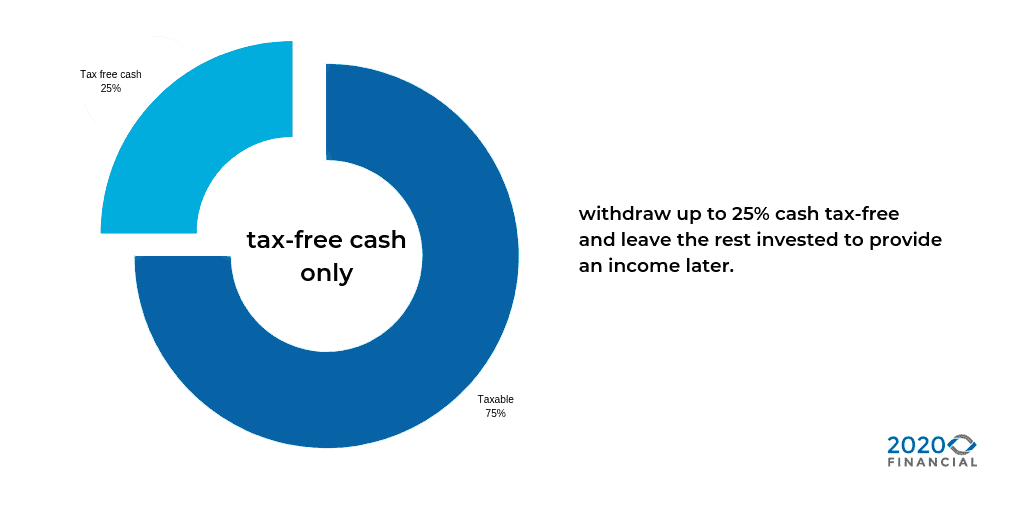

Pension reforms introduced in 2015 allow you to access your private pension from age 55 (moving to 57 from 2028). These reforms also gave private pension holders access to 25% of their pension as tax-free cash that can be taken as a lump sum, in chunks or as part of a blended income.

If you have a defined contribution pension there are a number of ways that you can take your pension at 55 and still work. You can opt to take it in a single lump sum, take smaller cash lump sums, you can even start paying yourself a regular income from your pension.

If you have a guaranteed pension amount in the form of a defined benefit pension then the rules around when you can start taking your pension are different and you’ll need to check with your pension scheme administrator to find out what applies to you.

Can I work and take my pension?

In most cases, under current pension and employment rules, you can work and receive your private pension at the same time. Most of the time pension schemes are not operated directly by the employer so you won’t need to inform them. In the case of defined benefit pensions you will need to check the rules around working and claiming your pension with your scheme provider.

Pensions count as taxable income so be aware that the added pension income may push you into a higher income tax bracket.

If you continue to work full time and you have no need for the additional pension income, you may want to defer taking your private pension until you stop working or reduce your hours.

The default retirement age of 66 no longer exists, so your employer can’t force you to retire at a certain age. Even if you start taking your pension early, you can’t be forced to retire when you hit 66 unless there’s another law that requires it, or your job requires you to have a certain level of mental or physical abilities i.e. firefighters, pilots etc.

How much can I take out of my pension at 55?

You can access your entire pension pot from the age of 55 and there’s no limit to the amount you can withdraw. 25% is tax-free, anything after that is taxed at your marginal rate. However, any withdrawals you make at 55 could impact your retirement plans and long-term financial future, so you should consider the long-term impact of your decision.

If you do take your pension pot in one go you may be faced with a hefty tax bill for doing so and you’ll also have to have a plan as to how you will fund the rest of your retirement. It’s worth noting even if you get the full state pension it’s unlikely to be enough to afford even a basic standard of living in retirement.

Many people opt to take their 25% tax-free cash at 55 to facilitate early retirement, pay off a mortgage, pay for a holiday etc but it’s important to note that 25% of your pension is a large chunk to take in one go and it might leave you wanting in later years.

As a general rule if you want to ensure that your pension pot does not run through your retirement you should aim to take no more than 4% of the value of your pension in any one year.

4% is the amount designated as the Safe Withdrawal rate; The rate at which your investment should increase in value in line with your withdrawals, effectively cancelling your withdrawals out and retaining the value of your pension pot over the long run.

If you’re thinking about accessing your pension at 55 it’s a good idea to talk your plans through with a financial advisor who can help you balance your short, mid and long-term goals with your short, mid and long term needs.

read more in what’s a good retirement income

Phased Retirement vs Semi-Retirement

Phased retirement and semi-retirement involve reducing your working hours and mirroring your chosen retirement lifestyle in the time you have off. with a phased retirement you may choose to cut your hours down gradually, for instance, moving to a four day work week then to a 3-day work week etc. alternatively, you may reduce your hours down and then up to become a consultant to your previous company but the idea is that you ultimately work towards full retirement.

Semi-retirement is slightly different in that you split your time between work and retirement lifestyle on an ongoing basis. if you enjoy working you might decide that permanent semi-retirement works for you. you effectively work part-time and enjoy it all the trappings of retirement in your time off. if you don’t have adequate retirement savings semi-retirement may provide a workable solution for you to enjoy it a comfortable living standard in retirement.

How much can I drawdown from my pension without paying tax?

Nobody wants to pay more tax than they need to, and if you’re working and taking money from your pension it’s important to understand the tax implications of doing so and plan effectively so you don’t end up with an unexpected tax bill.

Technically you could draw down your entire pension without ever paying tax if you take advantage of your 25% tax-free cash and keep your income within your tax-free allowance amount.

However, if you’re working and taking money from your pension it’s likely that you’ll exceed your personal allowance. Since pensions count as taxable income.

In order to minimise your tax liability whilst you’re working and taking your pension you’ll want to:

- Make use of your tax-free cash

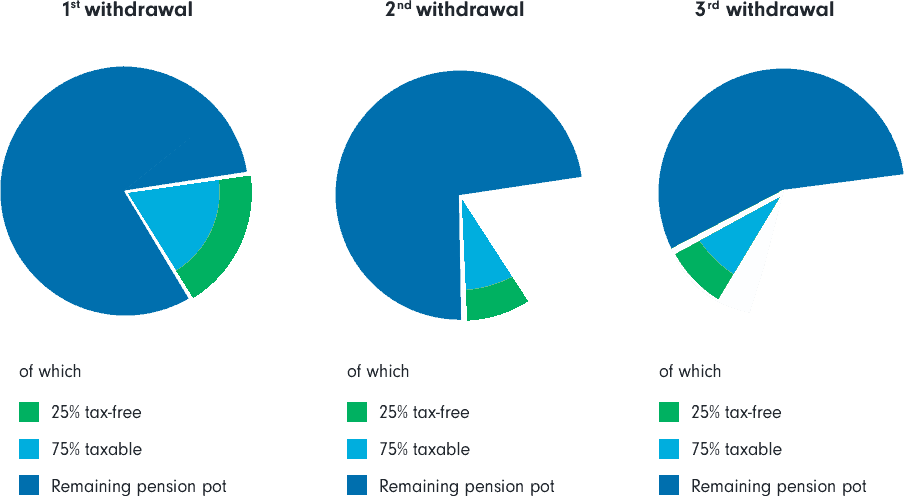

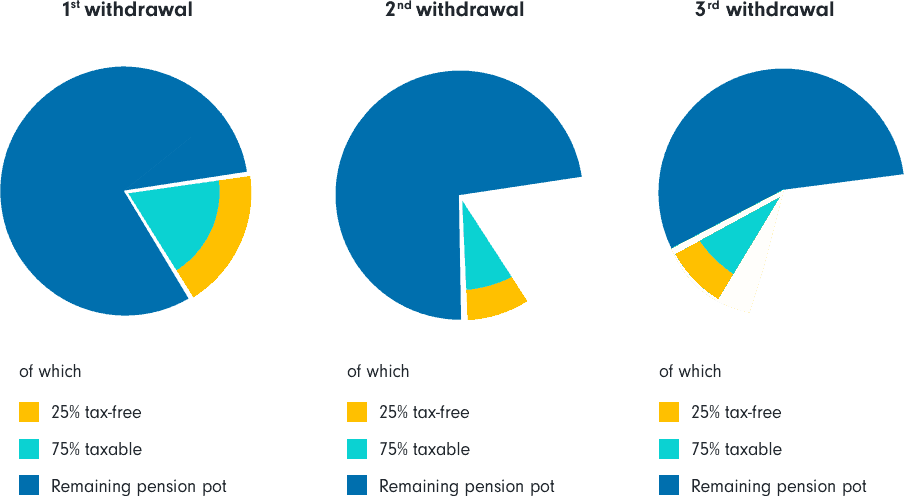

You can draw down 25% of your pension tax-free – after this, the remaining 75% is liable to be taxed at your highest amount.

You don’t have to take all of your tax-free cash in one go, so it can be phased and blended with other income to minimise your tax liability.

- Make use of your tax-free allowance

Every year you have a zero rate tax allowance, known as your personal allowance, this is the amount that you can earn up to before you pay tax. If you keep your pension withdrawals and total income below this amount you will not have to pay tax on your pension withdrawals.

The current tax-free allowance for 2021/2022 is £12,570 per year. So, if your pension drawdown is your only income – and you aren’t earning anything else – you could withdraw this as a tax-free sum across the span of a year.

3. Blend your tax-free cash and taxable income

Rather than taking all of your tax free cash in one go, you can blend your tax-free cash with income to maximise legal tax-breaks and minimise your taxable income whilst you’re still working.

This is something that your Financial Advisor will be able to help you with – because it isn’t a clear cut answer, and there are certain ways to be more efficient when it comes to the tax implications of your drawdowns. For example, while you may choose to take your 25% tax-free allowance one year, you always have the option of utilising your yearly tax-free allowance in later years.

Try our favourite pension tax calculators to see how much tax you might pay on your withdrawals.

Should I take my pension at 55 and still work?

If you are looking to take your pension at 55 and still work there are a number of things to consider:

- The impact and withdrawals will have on your pension pot

- Will you have enough money to last you in retirement if you take your pension at 55?

- How much tax you’ll pay and whether it’s best to keep your pension invested

- What will you do if you can no longer work i.e. due to ill health or redundancy

- Are there other options available to you? i.e. savings, cash from the sale of your house?

- Money Purchase Annual Allowance – will this affect you?

- Are there more tax efficient ways to fund your retirement?

- Inheritance tax planning – do you want to leave an inheritance for family or loved ones? How will reducing your pension pot affect this?

It’s worth speaking to a financial adviser to put a retirement plan together. Our advisors have helped hundreds of people like you plan for an early retirement.

How can I take my pension and still work?

The pension freedoms introduced in 2015 now allow you to access your pension in a number of ways at 55, even if you are still working. If you have a defined contribution pension you can:

- Access 25% of your pension tax – free and leave the rest of your money invested

- Take some or all of your tax-free cash and buy an annuity with the remaining pension pot

- Purchase an annuity with your whole pension pot

- Access your pension pot flexibly through flexi-access drawdown (here’s what we believe to be the best pension drawdown calculator)

- Put it into flexi-drawdown and take a monthly income (taxable)

- Take your pension in lump sum chunks

- Take your tax-free cash in phases

Or combine some of these options.

This might sound complicated. But, basically, with a defined contribution pension, you can take as much, or as little as you need. As and when you need it.

When you’re ready to start taking money from your pension contact your pension scheme to arrange a withdrawal or to set up a regular payment (be aware this may trigger the Money Purchase Annual Allowance and additional tax liability). If you’re unsure about any of these things it’s best to speak to a financial advisor for advice before you make any decisions on your pension.

If you have a defined benefit pension (Final Salary Pension), once you start taking your pension you have to take the full amount every year. If you take it early, the amount you receive every year will be reduced and if you’re entitled to a tax-free lump sum, that might be reduced too.

The amount you have to give up to take early retirement depends on the rules set by your pension scheme. Contact your pension scheme administrators to find out what rules apply to you.

You should speak to a financial adviser before deciding whether or not to take early retirement from a defined benefit scheme, especially if you plan to continue to work as there could be tax implications of taking your pension and continuing to earn an income at the same time.

Do I pay tax on my pension?

Unlike national insurance, which you stop paying when you reach State Pension Age, you will pay income tax even after you retire – regardless of your age, even if that income is from a pension.

You’ll have your annual tax allowance which is set at £12,500 for 2019/2020. But after that you’ll pay tax .

You can take advantage of investments held in ISAs to provide a tax-free income on top of this. You can currently invest up to £20,000 a year into an ISA and any increase in value or dividend you receive from your investments held within the ISA can be taken tax-free.

Pension lump sum

With the pension freedoms of 2015, if you have a defined contribution pension, you can now take your pension as a series of cash lump sums the first 25% will be tax-free with the rest taxed at your marginal rate. These are known as UFPLS (pronounced uff-plus) or FLUMPS and it stands for Uncrystallised Funds Pension Lump Sum.

Source: Fidelity

Most people opt to go into flexi-access drawdown over taking one off lump sums because of the flexibility it offers to blend tax-free cash and taxable ‘crystalised’ pension income. If you want to know what’s right for you. Talk to one of our financial advisers.

Tax on pension lump sums

The first 25% of your pension pot is tax-free and the rest of your Pension is taxable. If you plan to carry on working and take income from your pension at the same time, you will need to factor in how much tax you’ll pay. Talk to a financial adviser, as there may be tax efficient ways to take money from your pension.

Click here to find more information about taking a lump sum from your pension.

Want to know how much tax you’ll pay on the cash you take from your pension? We’ve pulled together 5 of the best pension lump sum tax calculators

Money purchase annual allowance

You can continue working for your employer whilst taking your pension but if you want to continue to fund your pension whilst you work you may run into problems. There’s a limit on how much you can pay into your pension once you have started taking an income from it – it’s known as the money purchase annual allowance (MPAA).

Pensions are a tax efficient way of saving. You get tax relief based on your highest level of tax so if you want to continue to build up your pension pot, you need to be careful not to trigger the Money purchase annual allowance.

The Money Purchase Annual Allowance MPAA is a limit on the amount you can pay into your pension and receive tax relief on.

The amount you can pay into a pension and still claim tax relief drops from £40,000 a year to £4,000 (2019/2020 allowance) once you trigger the MPAA.

Once it’s gone. It’s gone! Once you’ve triggered the Money Purchase Annual Allowance you can’t go back to putting a higher amount in, even if you stop working!

Related: How much do I need to Retire at 55

Final Salary Pensions and early retirement?

Final Salary or Defined Benefit Pensions are not governed by the same rules as Defined Contribution pensions. How and when you can access your tax-free cash or a lump sum are decided by your pension scheme and vary from one scheme to another. You will need to check with your own scheme for their rules on lump sums.

You will also need to check with your scheme to find out if early retirement is possible and how much your pension and/or tax-free cash will be reduced by if you opt for early retirement.

Many of the pension freedoms announced affect final salary pension differently. If you have a final salary pension and want to find out more check out our blog : 9 New Rules for Final Salary Pensions You Need to Know About. If you want more flexibility than your current pension can offer then you could consider a Final Salary Pension Transfer

Next Steps

Before you start planning your retirement it will help to have an understanding of how much income you’ll need. We’ve put together a simple retirement cost calculator for couples and separate retirement calculator for singles

We also recommend reading How much do I need to retire and What’s a good retirement income.

If you’re ready to make your early retirement dream happen, book a consultation with our experts and we’ll help get your financial plans in place to put the wheels in motion.

{kind=link}