Slow, lazy mornings, sun-filled afternoons with your loved ones and an endless bucket list… Sounds pretty sublime, right? And now that you can access your pension from the age of 55, you might be wondering if you can retire early and reap all of those incredible benefits as soon as possible. But can you really afford to do it? Exactly how much do you need to retire at 60?

The minimum recommended income in retirement is £9,609 a year so if you retire at 60 you’ll need roughly £57,500 in income to last until your state pension kicks in 66. After that you’ll need at least £300 a year in personal income to top up the full state pension to a minimum income standard.

N.B. The current state pension age is changing, for some of us, we won’t receive our state pension until we’re at least 68.

These estimates assume that you’ll be comfortable living on the minimum amount recommended for retirement… And this really is the bare minimum. That means no dog, no car, no trips abroad. It’s retirement in its most basic form.

However, if you’re hoping to enjoy a comfortable retirement experts estimate you’ll need between £15,000 to £40,000 a year (or if you’re using Target Replacement Rate as a measure, you’ll need between a half and two-thirds of your pre-retirement annual income every year).

Saying that, retirement is no longer a one size fits all situation and a comfortable retirement for one person could be an abundant one for another.

£40,000 might feel like a huge amount of money to you, on the other hand, it might not even cover your annual travel budget…It’s all relative. But for the purposes of this article, we’ll assume that you’re an average person in the UK and that you are happy to retire on £15,000 to £40,000 a year.

In this case, you could need anywhere between £90,000 and £240,000 to retire at 60, and that only gets you to state retirement age. You’ll still need to budget to top up your state pension once you get to state pension age.

Fundamentally, how much you need to retire at 60 depends on the standard of living you want for your retirement, your personal financial situation and when you’re due to receive your state pension.

Should I retire at 60?

If you want to – and you can do so comfortably – then why not? There are so many different types of retirement that you can take (read our blog on the six types of retirement here), and many of these allow you to work considerably fewer hours while drawing your pension.

The benefits of working fewer hours isn’t a new concept; it’s acknowledged that those who work fewer hours experience lower levels of stress and better wellbeing. But, it’s also been argued that a three-day working week is optimal for those over 40 when it comes to improved cognitive function.

Ultimately, it all comes back to making sure that your pension pot can support you throughout your entire retirement – what may seem like a good idea now could end up leaving you high and draw years down the line. That’s why it’s crucial that you consult a financial advisor before making any final decisions, as they will help you create a clear strategy and cash flow analysis so that you know how long your pension pot will really last.

How much money do you need to retire at 60?

The quick answer? It depends. The long one? You’ll need between one half and two-thirds of your pre-retirement income to be comfortable, but you’ll also need to consider any changes in your income and outgoings as you reach your golden years (plus, whether a ‘comfortable’ retirement is actually what you want).

And there’s more. How much you need in your pension pot is generally decided by:

How much you need in annual retirement income (X multiplied by) The length of your retirement

Unfortunately, we can’t predict the future and so it’s impossible to know how long you will live, yet we can work with some industry-accepted assumptions to give us a reliable foundation for a retirement plan. You may also want to use a life expectancy calculator, which works on averages based on gender and age.

We asked Simon Garber – our retirement planning specialist IFA – how much you’d need in your pension pot if you’re planning on investing your money and using pension drawdown to retire at 60, he said:

“As a rule of thumb, for every £3-4K you plan to take in annual income, you’ll need about £100,000 in your pension pot. So if you opt to take £10K per year, you’ll want roughly between £250-£330K in your pension pot.”

Obviously, once you hit state pension age, you should start to receive your state pension income as well (check your eligibility here), which means you won’t need to find quite so much money from your private pension or other income sources.

What type of retirement do you want?

Not all retirements are created equal. Another factor to consider is what type of retirement you want. The six main types are:

- Mini-retirement

- Permanent semi-retirement

- Early retirement

- Phased retirement

- Traditional retirement

- Ill-health retirement.

Your chosen retirement will impact the amount necessary for you to comfortably retire at 60 – this is something your financial advisor will be able to guide you through.

What’s a good retirement income?

A good retirement income is one that allows you to have a comfortable retirement free from stress and financial concerns.

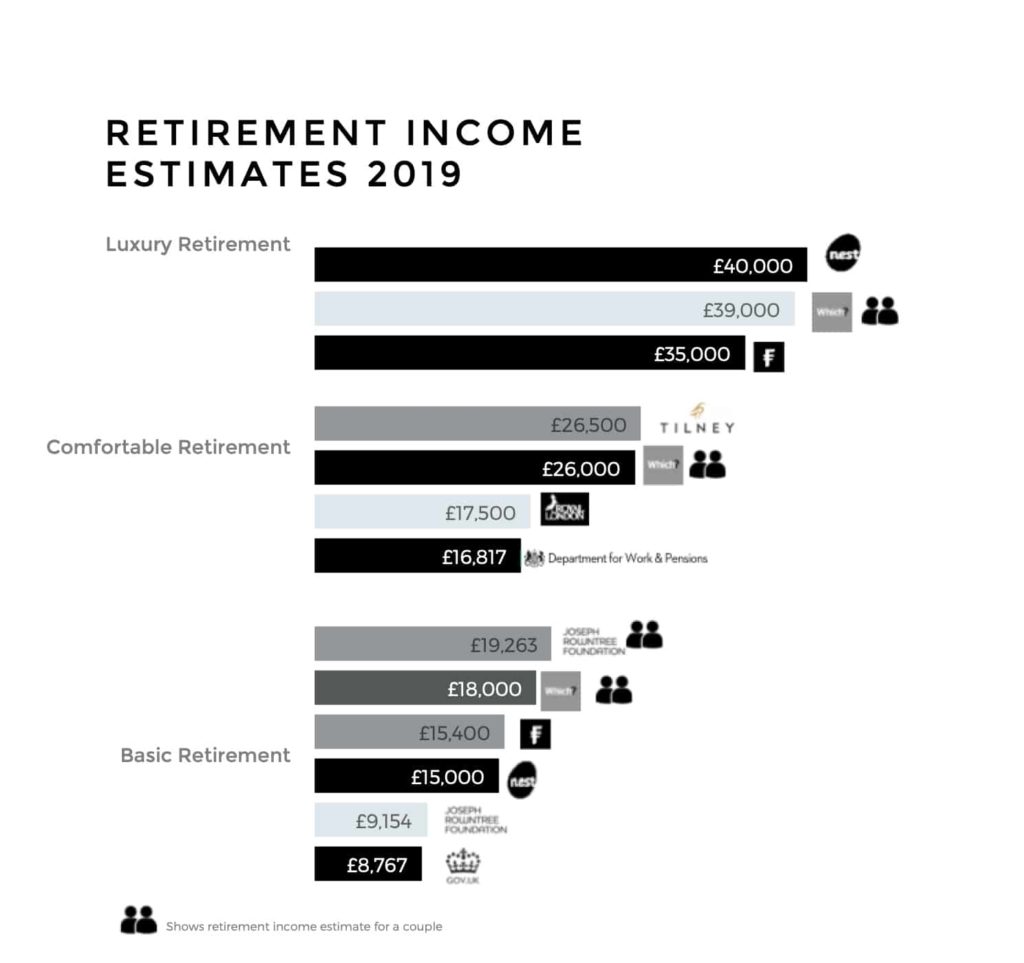

Estimates for what is a good retirement income vary wildly; for example, are you a single person or a couple? How much did you earn before retirement? There are rule-of-thumb figures that make a useful place to start, as shown in the graphs below:

The minimum recommended income in retirement for 2020 is £9,609 for a single person and £18,779 for a couple, According to research by the Joseph Rowntree Foundation, this amount, after tax and benefits adjustments, is enough to cover what the public think is needed for a minimum decent standard of living.

In comparison, research by consumer group Which, place the cost of a comfortable retirement for a couple at £25,000 per year and a luxury retirement (with long haul holidays, gym membership and a new car every 5 years) will set you back approximately £40,000 a year.

You can calculate your own retirement target by using our retirement cost calculators. Click here for singles and here for couples. Once you have a rough figure in mind, you can start to create a bespoke retirement plan – this is something that your financial advisor will support you with.

How to retire at 60?

If you have a defined contribution pension, you can access your pension from the age of 55 – so as long as you have enough saved retiring at 60 is simply a case of handing in your notice and starting to drawdown your pension.

Remember, you can access 25% of your pension pot tax-free, but if you draw down over 25% it will be taxed at your highest marginal rate of tax.

This will be added to your overall income: in the eyes of the taxman – once you pass £50,271 – this could very quickly see you move into the highest rate tax bracket.

When it comes to minimising your tax liability, it can make sense to use a blended approach, combining your tax-free income allowance with the tax-free cash in your pension pot.

If you want to retire at 60, you will need to ensure that you have the money set up to provide you with an income for the rest of your life or – at the very least – until your state pension comes in.

If you retire at 60, you’re extending the length of your retirement. It’s important when you do this that you don’t treat all of your retirement savings as if they’re needed right away, make sure that you leave enough of your pension pot invested appropriately to provide an income in later retirement.

Of course, if you haven’t got enough money saved for retirement at 60, you might still be able to enjoy a more flexible approach to retirement that offers you some of the freedom you crave, with less of the cost. Check out our article on the different types of retirement.

Can I take my pension at 60 and still work?

If you haven’t quite built up a large enough pension pot to fully retire at 60, there are other options.

Now that pension freedoms allow greater flexibility, there are plenty of different types of retirement for you to consider. Permanent semi-retirement, mini-retirement and/or phased retirement offer the freedom to take some of your pension early, while still working part-time, so you can enjoy some of the benefits of retirement without depleting your pension pot prematurely.

Keep in mind that once you start to take an income from your defined contribution pension you will trigger the Money Purchase Annual Allowance, which limits the amount you can put into your pension and receive tax relief on.

It’s a complicated area, and one you should seek financial advice on if you’re thinking about working and taking your pension at the same time. Your financial advisor can build this into a long-term forecast for you so that you know exactly where you stand before making a commitment.

Will I get the state pension if I retire at 60?

Your state pension (if you’re eligible) isn’t paid until you reach state pension age, regardless of what age you choose to retire. The current state pension age is 66, but it’s moving to 68 and it differs depending on when you were born. Check for free on the government website to see when your state pension is due so that you can feed this into your pension planning.

So if you retire at 60, there are currently at least 6 years of retirement you will have to fully fund yourself.

How much do I need to save to retire at 60?

How long is a piece of string? The amount you will need to save to retire at 60 will depend on your definite outgoings (such as bills, groceries, rent, mortgage repayments etc) and also your creature comforts. The best way to figure out the amount you need to save is to curate your overall figure first, and then work backwards.

Deciphering how much you should save every month to retire at 60 depends on three core factors:

- When you started saving

- What investment return you can expect

- How much you currently have in your pension pot

It won’t come as a surprise that the earlier you start to save, the less you’ll need to save monthly and the more time you’ll have to benefit from the plethora of pension pot returns.

You can use our How Much do I Need to Retire Calculator for straightforward calculations that will help you budget for your golden years. For bespoke advice, get in touch with a member of our friendly team.

As a general rule, for every £3000-£4000 you need in retirement income, you’ll need to have saved roughly £100,000 in your pension pot. So if you want £15,000 income every year on top of your state pension, you’ll need anywhere between £375,000-£500,000 invested.

How to Fund Your Retirement at 60.

There are several different options to fund your retirement at 60:

- Access your private pension from 55 – use flexi-access drawdown or buy an annuity

- Tax-free cash from your pension

- Rental income

- Dividends from a business

- Money from the sale of a business

- Money from the sale of a property

- Savings and ISAs

- A redundancy package

- A maturing endowment policy

- An inheritance

- Opting for a flexible working retirement or

- Part-time work – read 7 jobs you can do in retirement

Again, your financial advisor will look at all of your different income sources and use them to create a sustainable financial plan to help you access the retirement of your dreams.

Factors that can affect retirement cost.

There are plenty of factors that could affect your retirement income needs; these mean that you may need to adjust as you move along.

To start off with, you can confidently accept that you will need a larger pension pot if:

- You have a low rate of return on your investments or you want to minimise risk in your investments

- You retire early and increase the length of your retirement

- Your retirement income is indexed to inflation

- You’re not entitled to the full state pension

- If you don’t own your own home or you haven’t cleared your mortgage

- You have planned capital spending i.e. to buy a motorhome, home renovations, gifting money to help a child or grandchild buy a home etc.

- You are the sole breadwinner and therefore need more of a contingency

One of the biggest factors impacting your retirement is whether or not you own your own home. It is estimated by Royal London that a third of retirees will eventually be renting and will typically need to find an extra £6,554 a year in retirement to pay private landlords, equating to a pension pot of at least £445,000. And that’s based on retiring at the State Pension age! If you choose to retire early at 60, you’ll need to find a way to fill the gap between when you retire and when you receive your State Pension.

Alternatively, you can get away with a smaller pension pot if:

- You retire later

- You earn a higher rate of return on your investments

- You lower your income expectations at retirement

- You have alternative income streams (i.e. part-time work, passive income or property rental)

- You are able to downsize and partially fund your retirement with the equity

- You have a partner with a large pension that can provide for you both

- You are in poor health with a reduced life expectancy

Can I retire at 60 with 500K?

Sure, £500K may sound like a decent amount of money but it might not provide you with the luxurious lifestyle you were hoping for if you plan to retire at 60.

If you retire at 60 with £500k in the UK, you could reasonably expect to take between £15-20K from your pension every year.

That’s teetering on the edge of the £19,000 Which suggests you’ll need as a single person to enjoy a comfortable retirement and less than half the amount a couple would need for a comfortable retirement.

Of course, if you are eligible for the full state pension then you can add about £9300 a year to that amount, which starts to make the figures look a bit more comfortable.

It all comes down to the type of retirement you want to experience.

Can I retire at 60 with 600K?

Even with another £100k in your pension pot, you may not access the retirement of your dreams. If you retire at 60 with £600k in the UK, you will take between £18-24K from your pension every year – certainly a more attractive income, but still far away from a luxurious retirement.

Even if you’re in a couple and you both get your full state pension, at the best estimate you’ll have around £42,600 income in retirement. If you’re used to having more disposable income than that, even a £600,000 nest egg might not seem generous enough.

Can I retire at 60 with 700K?

Retiring at 60 with £700k will give you a retirement income of around £21-28K. This would give you a secure retirement, and one that is on the verge of moving from comfortable to luxurious. However, this will largely come back to what ‘comfortable’ and ‘luxury’ really means to you, and how you want to experience and enjoy your later years.

If you plan on helping children onto the property ladder, or you want to purchase a holiday home for your retirement, you might find that even £700,000 in your pension pot could leave you short.

Of course, if your needs are modest, a £700,000 pension pot might be more than you could ever spend.

Can I retire at 60 with £1million?

There’s something comforting about £1million. It feels like the kind of money that could last you forever.

The reality is that retirement is a long time to have to stretch your savings and even £1million might not be enough to give you the dream retirement you’re hoping for.

Retiring at 60 with £1million could reasonably give you a sustainable income in retirement of between £30,000 to £40,000 per year if you stick to a safe withdrawal rate of between 3-4% of your pension pot.

If you are banking on your full state pension to kick in at 66-68, you may be able to take a little bit more – however, avoid taking too much from your pension pot too soon as you could risk running out of money prematurely.

It’s best to speak directly to a financial advisor who can then show you how your withdrawals might affect your pension pot over time.

And that’s where we can help. Simon is a pension and retirement specialist with over 15 years of experience. His advice is 100% impartial and based on a successful career delivering high-quality, person-centred, tailored financial advice that helps clients reach their financial goals.

Schedule a call today and get your retirement plans on track.

{kind=link}