In 71% of UK divorces Pensions are not discussed, in fact as it stands, unless you go to court there’s no automatic right to even know how much your spouse has in their pension, so it’s unsurprising that many people going through a divorce don’t know how much of their spouses pension they are entitled to in a divorce; So how much of your husband’s pension are you entitled to when you divorce?

In the UK pensions count as a joint marital asset and should be split during a divorce. They can be split in a number of ways: They can be shared or the value may be offset against other assets, but the starting point should be a 50/50 split of all assets including pensions.

Am I entitled to my husband’s pension when we divorce?

Yes, but because of the way assets are divided in a divorce, you may not always receive part of your husband’s pension. That might sound contradictory but it is because of the way Divorce settlements are worked out in the UK. On your divorce, or dissolution of your civil partnership, all of your assets and those of your ex-spouse or partner are taken into account.

Pensions that can be split in Divorce include

- Personal pension scheme

- Schemes you have through work and old workplace pensions

- Additional State Pension (but not the basic State Pension)

Pensions can be split in 3 ways:

- Pension Offsetting

- Pension Sharing

- Pension Attachement/Earmarking

Pension Offsetting

UK Divorce courts favour a 50/50 split that provides a clean break for both parties and they will first consider the needs of any children.

Often this means that the main caregiver of any children will often receive the marital home (or a larger share of it) and the other spouse may receive other marital assets – cash and/or pensions.

In this way – the value of the Pension is offset against the value of other assets. This is the only way of splitting a pension in divorce that doesn’t require a court order.

Pension Sharing

A pension sharing order entitles you to a percentage of any one (or more) of your ex-partner’s pensions. This is usually transferred into a pension in your name or you may be able to join your ex-partner’s pension scheme.

You can agree a pension sharing order through mediation or your own solicitors it might be signed off by the court. As you will need a court order to set up a Pension Sharing order.

If you cannot agree a pension sharing order between both parties, you will need to go through the courts, which can be a lengthy and expensive process.

Find out more about pension sharing in our pension sharing orders post.

Pension Attachment/Earmarking

Although courts no longer favour Pension Attachment orders or ‘Earmarking’, they are still an option; they don’t offer the ‘clean break’ solution that Offsetting or Pension Sharing Orders do.

You are awarded a share of your ex-partner’s pension but you cannot access it until they start to take their pension. You can get some of the pension income, the lump sum or both. However, if you’re divorcing after your partner has retired it’s not possible to take a lump sum from your ex-partner’s pension if they are already receiving an income from it.

Pension Earmarking if your Spouse is a Divorcee

It’s important to know that if your spouse has been divorced before and already has a Pension Attachment or Pension Earmarking order on their pension, then it is not possible to subject that earmarked portion to a further earmarking order.

A Pension Attachment order can only be applied with a court order. It can’t be applied as part of an out of court settlement.

Try our Pension Divorce Calculator to see what you might be entitled to in a Divorce.

Will a wife always get half a husband’s pension in a divorce?

No. In fact in 7 out of 10 divorces, pensions aren’t even discussed, let alone split in a divorce. In DIY divorces or online divorces there is no financial remedy and a pension sharing orders cannot be made. Often because Pnsion assets aren’t obvious to both parties in the divorce, they get missed

If you are going through mediation, it is important to make sure that pension assets are raised and full disclosure of the value of pensions is made.

In Scotland the rules surrounding pensions and divorce differ from the rest of the UK. Only the value of the pensions you have both built up during your marriage or civil partnership is taken into account.

For England, Wales and Northern Ireland the total value of the pensions you have each built up is taken into account. This means not just the pensions that you or your ex-partner built up while you were married or in a civil partnership, but all of your pensions – except the basic State Pension, even if they were accrued before the marriage.

There are a number of mitigating factors that may be taken into account that might affect how much of your husband’s pension you might receive in a divorce including your age, your spouse’s age earning potential, length of marriage and also how close you both are to retirement.

For instance, if you are significantly younger than your husband and he is close to retirement, a court may argue that his need is greater than yours and that you have the earning capacity and opportunity to build your retirement fund.

In the case of Pension Offsetting a court may not judge the value of an asset such as a house in the same way as they value a Pension, especially if the pension cannot be accessed for a number of years. Someone with a pension may also need to pay tax on it, unlike the person receiving the property.

How much of your husband’s pension are you entitled to after a divorce?

Pension wealth forms part of a couple’s joint assets in a divorce under UK law and should be split accordingly.

Divorce settlements in the UK are usually based on a 50/50 split of marital assets but this may not always be the case, especially when there are children involved, if it is a short marriage or if the bulk of the pension or wealth was built up prior to the marriage.

Courts will attempt to agree a fair settlement to both parties and so a 50/50 split may not be achieved.

Factors that can impact the share of any assets in divorce include:

- Children – their financial needs as well as other factors that may affect their future wellbeing;

- The financial needs of you and your spouse

- The length of the marriage and your respective ages;

- The current earnings of each party and the potential earning capacity of each party now and in the future;

- Health issues affecting either you, your spouse or any children;

- The assets of each party including pensions;

- The standard of living you have had during the marriage;

- The financial and non-financial contributions (such as caring for children and running the house) that each of you has made to the marriage;

Source: Teeslaw.com

Discover the full list of factors that can be assessed as part of the Matrimonial Causes Act 1973 here.

Private pension/s, workplace pension/s and/ or additional State pension (but not the basic state pension) can all be split as part of a divorce settlement.

If you’re in England, Northern Ireland or Wales, it is usually the total value of combined pensions that is taken into account. In Scotland, it is just the value of pensions accrued during the marriage that counts towards the marital assets.

The value of any pensions should be added to the value of any other marital assets including property, businesses, bank and savings accounts that you have and then you’ll need to agree how they are to be split. If you are going through mediation you’ll need to have your agreed settlement signed off by the court.

So, in theory, you should get half the value of your husband’s pension as part of your divorce but it will depend on the factors named above and how you decide to split your marital assets as to how much you receive and whether you receive a share of the pension or other assets equal to that value.

The most common ways for pensions to be split in divorce are Pension Sharing orders and Offsetting.

With a Pension sharing order, the court would order a portion (or all) of your husbands pension to be handed over to you. You may have the option to join your ex-husband’s pension scheme, but more likely you’ll need to set up a pension of your own for the money to be transferred into.

How to calculate the value of a pension in a divorce?

Pensions are valued by their Cash Equivalent Value, which the pension holder will need to request from their pension trustee. It is also important to know whether the pension comes with any guaranteed cash lump sums or other valuable guarantees.

It is highly likely that you’ll have built up more than one pension over your working life, you’ll need to include details of all of your pensions. If you have old or lost pensions you can use the government’s free pension tracing tool to find the details of pension trustees and you’ll need to contact them directly to see if you have a pension held with them.

At the moment, unless you go to court, there is no automatic right for either party to disclose the amount they have in their pension, so you will be reliant on your spouse disclosing the correct amount. There are ways in which you can protect a pension during a divorce (read here).

Calculating the value of a Final Salary Pension in Divorce

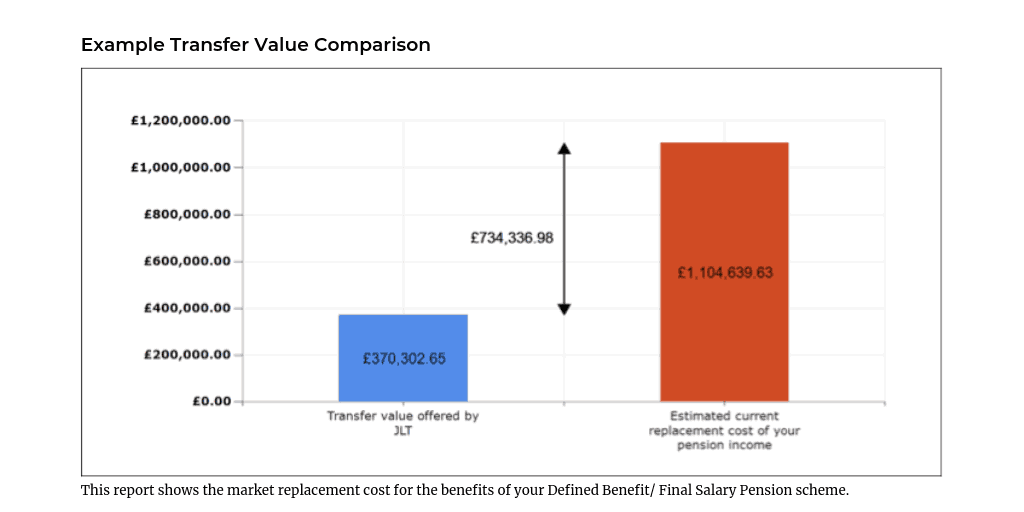

In the case of Final Salary or Defined Benefit schemes the Cash Equivalent Transfer Value may be used – however it’s important to note that the Cash Equivalent Transfer Value rarely reflects the true market value of this kind of asset. Final Salary Schemes offer extremely valuable, life-long guaranteed income that is protected against inflation, they also include a provision of a survivors pension for life for a spouse and may also include protected early retirement guarantees – It is rare that these kinds of benefits and guarantees can be replicated like for like with the Cash Equivalent Transfer Value.

Pension Transfer Specialists are required to use a calculation known as Transfer Value Comparison when assessing the true value of a Final Salary Pension. This gives you a realistic estimate of the value of any Final Salary Pension.

Try our Pension Divorce Calculator to see what you might be entitled to in a Divorce.

If your spouse works for the military, police, NHS, fire service or has a teacher’s or local authority pension, then it may be worth asking the court to consider a Transfer Value Comparison rather than a standard CETV.

Whilst you would need to pay for a specialist adviser to provide this kind of analysis, as you can see from the model above, the true value of a Defined Benefit/Final Salary Pension is likely to be much higher than its Cash Equivalent Transfer Value suggests and it may be in your interests to get a fair estimate of what your spouse’s pension is actually worth.

Will I lose my ex-husband’s pension if I re-marry?

In the old days of Pension Earmarking, it was the case that if either spouse remarried the earmarking order became null and void.

However, with Pension Sharing and Pension Offsetting, this is not the case. Both Pension Sharing and Pension Offsetting enable a ‘clean break’ divorce and are not affected by subsequent marriages.

Pension Sharing orders effectively split the pension at the point of divorce and you will be in charge of any portion of the pension you receive. With Pension Offsetting, you receive other assets, i.e. a greater share of the marital home in place of the pension.

It is important to note that if you do opt for a Pension Offsetting arrangement, you should make sure that you have plans in place for your retirement.

Free Advice for Pensions in divorce

If you’re getting divorced it’s really important to get the right information. The information provided here is for your information only and is based on our understanding of current legislation, we are not solicitors and there’s no substitute for personalised advice for all things legal and financial. Divorce can be expensive but getting a bad deal could affect your long-term financial health. Here are some great free resources for you to start with.

Relate offer relationship support as well as divorce mediation and provide lots of free advice.

https://www.relate.org.uk/relationship-help/help-separation-and-divorce

The Pension Advisory Service provides free Pension Advice. You can book a free appointment to understand your pension options in Divorce, what you’ll need to think about and the things you’ll need to ask.

https://www.pensionsadvisoryservice.org.uk/

Advicenow.org

Advicenow is an independent, not-for-profit website, run by the charity Law for Life: the Foundation for Public Legal Education. They provide accurate, practical information on rights and the law in England and Wales.

Download their useful guides as a free PDF using the links below:

Survival Guide to sorting out your finances in Divorce

A survival guide to divorce or dissolution of a civil partnership

A survival guide to using Family Mediation after a break up

The Law Society

If you need help finding a suitable solicitor, The Law Society offers a free Find a Solicitor service.

Advocate

Advocate is a charity that finds free legal assistance from volunteer barristers. You can find out more about them and apply for help here.

Mediation

Search the Family Mediation Council register to find a mediator near you

Useful Divorce Calculators

https://www.iflg.uk.com/calculators/divorce-settlement-calculator

https://www.iflg.uk.com/guide/financial-outcomes

https://www.moneyadviceservice.org.uk/en/articles/divorce-and-money-calculator

{kind=link}