Investing for your retirement is a pretty easy thing to put off; afterall, you want to live your life and enjoy your hard-earned money, right?

Planning that far ahead can feel overwhelming. It’s a problem for ‘future-you’. Nothing to beat yourself about now. And when you’ve got countless other outgoings darting away from your bank account, the thought of yet another to add to the list is just exhausting.

Why is investing for retirement important? Investing for retirement early is your one and only way to guarantee financial freedom in later life. That means if you want to live out any of your future dreams, you’re going to want a carefully curated pension backing your corner.

Of course, it’s a little more complicated than that. Which is why we’re going to be digging deeper into the many reasons why you should make investing for your retirement a priority and why a retirement plan is important.

10 reasons you should start investing for retirement

1. The State Pension isn’t enough to live off

Let’s cut to the chase – you cannot comfortably live off the State Pension. In fact, you can barely live off it at all.

The current State Pension will give you a maximum of £175.20 per week. This should be seen as a top up to your other income, and an added extra to your pot of money. Relying solely on this would mean no holidays, no car, no shopping trips, no exciting new hobbies… basically, no fun.

And you deserve fun. You’ve worked hard for it. You should be able to enjoy those blissful years after you’ve put the 9-5 to bed, not scrape pennies together just for a Friday night takeaway.

It’s important to start investing for retirement early so you can mitigate for what is bound to be a low paying state pension.

2. The earlier you start the more your money can work for you

Did you know you can earn money from your pension interest?

It may sound like a bit of a riddle, but compound interest gives your investment the chance to really snowball. Plus, the longer you’re putting money into those savings, the higher your compound interest is going to be.

Picture this: whenever you earn interest on your retirement investment, that interest is added into your overall savings. But, the next time interest comes in, it not only is earnt on your original investment, but also the interest you have previously accumulated.

The longer you’re saving, the more you gain which is why a retirement plan is so important.

3. You want to retire early

Why wouldn’t you want to retire early? A handy wad of cash sitting in your bank. An exciting bucket list ready for you to explore. The world right at your fingertips. Who would want to wait for that?

If you do want to slip on the retirement jacket early, you need to make sure you have enough funds ready and waiting for you when you turn 55. This is the earliest point you can access your own pension, compared to your late 60s when it comes to a State Pension; an age that is rising year on year.

However, it’s important that you do your homework. Pinpoint the age you plan to retire by and make sure you know how much you need to save in that time to fulfil your lifestyle goals.

4. Immediate Return on Investment (through tax relief)

This is one of the best (and unique) things about investing into a pension: tax relief.

Tax relief means that whenever you make a payment into your pension, the government will boost the investment by repaying you tax at the highest rate you normally pay. Think of it as a reward for saving for your future.

It means that you have the potential to earn up to 40% extra money on your investment; a valuable tool to forecast into your overall saving timeline.

5. It’s free money from the government

The benefits of free money are fairly self-explanatory; but remember, you can only access those extra benefits if you make the investment.

The earlier you start investing for retirement is import, because and the more money you put in, the higher the input from the government. That means whether you’re a basic rate or top rate tax payer, you ultimately have control over how much free money will be funnelled into your pension.

6. It’s a free pay-rise from your employer

It isn’t just the government keeping your pension pot well stocked: thanks to auto enrolment, all employers now have to contribute, too.

This contribution is in addition to your salary, and it’s yours to keep far beyond your time with the company. The contribution will be added for every pay period that you pay into a work based pension, and you will be required to pay a minimum contribution as defined by your earnings. This will be topped up by your employer and the government tax relief.

However, we would always advise paying more than the minimum contribution so that you can reap more of the free money benefits!

7. If you’re Self-Employed it’s a tax-efficient way of deferring your pay

Despite there being over 5 million self employed people in the UK, less than a third of them are actively saving for retirement.

What they don’t realise, is setting up a personal pension when you’re self employed is a brilliant way of keeping your money safe ready for you to enjoy later and without any added tax payments on top.

It’s a tax-efficient way of paying yourself so that you get the maximum return later down the line Although you won’t get employer contributions, you’ll still be able to benefit from tax relief; therefore as with all pensions, the earlier you start, the better the final financial outcome.

8. If you’re a company owner pension contributions are a deductible business expense

As a business owner, pension contributions are a 100% legal, tax-efficient way of managing your company’s finances. Not only will your pension be protecting your money in the future, but it can actually make your life a whole lot easier right now.

That’s because any time you make a contribution – as a business owner – into your pension, you can claim it as a deductible business expense. You will then reduce your limited company’s Corporation Tax bill and boost the amount of money staying in your business account.

Don’t worry; this is far from a tax loophole. The rule was put in place to help business owners catch up with those in traditional employment since a high proportion of business owners will spend years with a reduced wage as they scale their business. It’s a totally legitimate way to draw together your future wealth while looking after your business’ tax liability.

9. You can take 25% of your pension TAX FREE when you retire

It is now possible to take a tax-free lump sum out of your defined contribution pension when you turn 55.And it isn’t a small amount: you can withdraw up to 25% tax-free, with the remainder classed as income. After that 25%, the rest of your investment will be taxed at your highest marginal rate. Due to this, if you do wish to take advantage of the Pension Freedoms rule, we recommend asking yourself the following questions before you withdraw further than the tax-free cash.

- How much tax will you pay?

- Will it impact you being able to continue paying into your pension?

- How will you fund your retirement?

- Will it affect the inheritance tax for your loved ones if you die?

10. Pensions aren’t subject to inheritance tax or capital gains

Inheritance Tax is tax placed on the estate (the property, money and professions) of an individual who has died. It is payable at 40% of any assets that exceed the ‘nil rate band’ threshold; this is currently £325,000.

The good news? Your pension sits outside of that.

Although your pension is an investment, it isn’t considered as part of your estate. As a result, if you die your pension can be passed onto anyone you wish and will not be liable for any inheritance tax payments. This can be a highly tax-efficient way of passing on wealth, and is frequently utilised by affluent individuals to pass on their money to children without the added inheritance tax deduction.

Why is it important to start investing for retirement early?

When it comes to saving for your retirement, the earlier you can start, the better.

You should approach your pension with an end goal in mind: how much do you need to not just comfortably, but happily retire and by what age? The ideal situation is to invest enough so that you can wave goodbye to work and retire early.

Even the smallest amount, bit by bit, can make all the difference if you start early enough. The later in life you kick off your investment, the more money you are going to have to squirrel away in order to hit your final finance goal; hence, a far bigger impact to your day to day life.

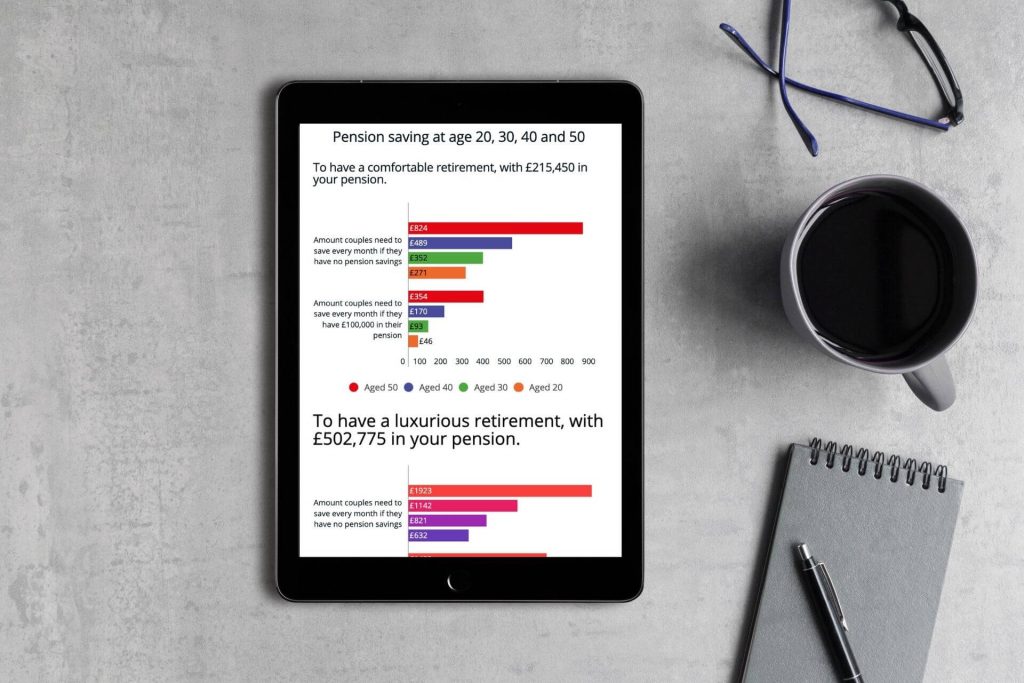

In fact, the difference between someone in their 20s and someone in their 50s kicking off their retirement investment and aiming for the same amount of money can be over four times as much in monthly contributions.

Plus, think of all those incredible free money benefits – surely you want to take advantage of them for as long as you can?

When should you start investing for retirement?

In a perfect world, you will start investing for retirement in your 20s. It may be the last thing on your mind at that age, but it is the best way to strategically grow your money.

There’s a general rule of thumb that says if you don’t start saving for your retirement until later, take the age you start your pension and halve it, then put this percentage of your pre-tax salary into your pension each year until you retire.

Our retirement expert, Simon Garber says:

“With something as important as your retirement and financial future, you don’t want to be dealing in rules of thumb. Especially If you’re starting late and playing catch up. it’s more important than ever to get the right advice from an expert.”

Fidelity caused outrage amongst millenials when they published research stating that in order to enjoy a comfortable retirement you should have saved 1x your salary by 30, 3x by 40, 6x by 50, 8x by 60, and 10x by 67. If you take into account pension tax-relief, employer contributions and investment growth, it doesn’t have to be as scary as it sounds.

Don’t panic if you haven’t started saving for retirement yet – it’s never too late. The key is to identify how much money you want to retire with, and then work with a Financial Advisor to work out the most clever, advantageous route to get there. You will also be able to explore the flexible options available and find one that best suits you: be this semi-retirement, phased retirement or one of the many other routes on the market.

Why is a retirement plan important?

Your Financial Advisor (here’s why you need one) will help you create a retirement plan that irons out all the details and fills in the gaps. This is crucial because there is no blueprint retirement plan that will work for everyone.

They will risk assess you and suggest a diversified pension fund plan to get the most out of your money. This will include making sure your money is invested in a mixture of assets to minimise your risk and help you grow your pot.

A retirement plan goes far deeper than a standard savings plan – there are many factors to consider and ways to ensure your investment hits a certain amount so that you can start earning an income off of it.

How should I be investing for retirement?

The best way to invest for your retirement is simple: you need to start your pension… and soon.

While it may seem like a problem to tackle in the future, before you know it those milestones will start ticking by and you’ll find it harder and harder to put that crucial money away. That’s why it’s vital to enlist the help of an expert to guarantee your retirement is fit for you and that your road to get there doesn’t burn a hole in your pocket.

Above all other saving options, your pension is the most tax efficient way to manage your wealth, and the prime tool for growing your money. Your pension will be subject to:

- Tax relief from the government (at the highest rate you normally pay)

- Bonus support from your employer

- A business expense as a company owner

It is important that you get a firm grasp on the benefits and how these will impact your contribution to your pension so that you know that the amount you are carefully saving is sufficient. A good place to start is with a pension calculator so that you can clearly pinpoint your current position – we’ve created one that is simple and efficient, making your first step as stress-free as we can.

Once you know your position, it’s time to maximise it. And that’s where we can really help.

Get independent pension advice

Your pension is likely to be the biggest, most important financial investment you ever make; you want to be sure that you’re getting it right.

There’s no magic bullet when it comes to pensions. Every individual will require something different. One roadmap will be opposite to another. And it’s easy to veer off the path and make some pretty big mistakes. Professional advice from a pension expert can keep you firmly on track.

At 2020 Financial we are experts in wealth management and retirement planning. We understand that we all have different dreams for retirement, and it’s our mission to turn those dreams into a reality.

Schedule a free discovery call with Simon to find out more about how we work and whether we are a good fit to help you protect your future finance.

{kind=link}