Planning your retirement as a single person can be a daunting task. You need to create a budget for the next 25+ years of your life. For things you may never have considered. The expected and unexpected costs. Dependents. Dreams. Hobbies.

On top of this, much of the available information focuses on couples, whose incomes, outgoings and tax breaks, all differ from your own. No wonder so many of us keep putting it off!

When considering a single person’s retirement needs, there are a number of considerations you need to take. Here’s our guide to how much a single person needs to retire on in the UK to allow for a comfortable lifestyle including different age brackets for 55, 60, and 66 (the current state pension age for both men and women).

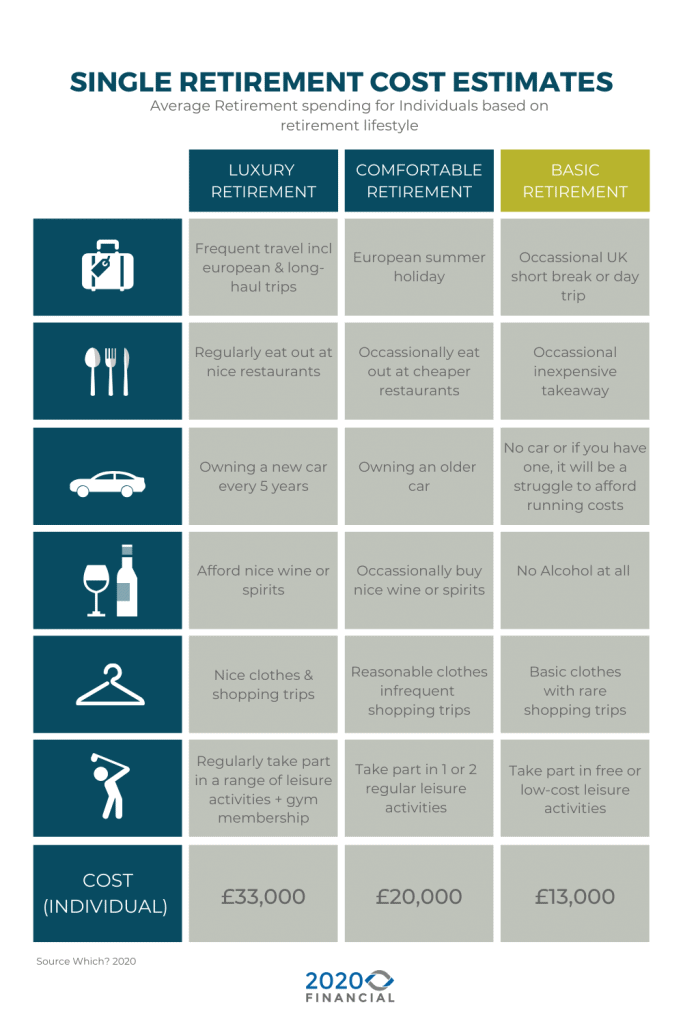

How much a single person needs to retire on depends on two things; (1) the age you want to retire, and (2) your income expectations. Research says you need £20,000 a year for a comfortable retirement with the basics and £33,000 a year for a ‘luxurious’ one. But it’s not quite this simple.

How much does a single person need to retire comfortably?

A comfortable retirement. What does that really mean? Comfortable for one person could be champagne breakfasts and private jets. For another, it’s golf once-a-month and a Sunday lunch at the pub. The idea of a ‘comfortable retirement’ is EXTREMELY subjective.

We are all different.

Which? says that a comfortable retirement for a single person costs around £20,000 per year. This includes European Travel/holidays, Buying new clothes and Recreation/Leisure.

Their estimate for a luxurious retirement for a single person costs around £33,000 per year. Including eating out, leisure membership and long haul travel.

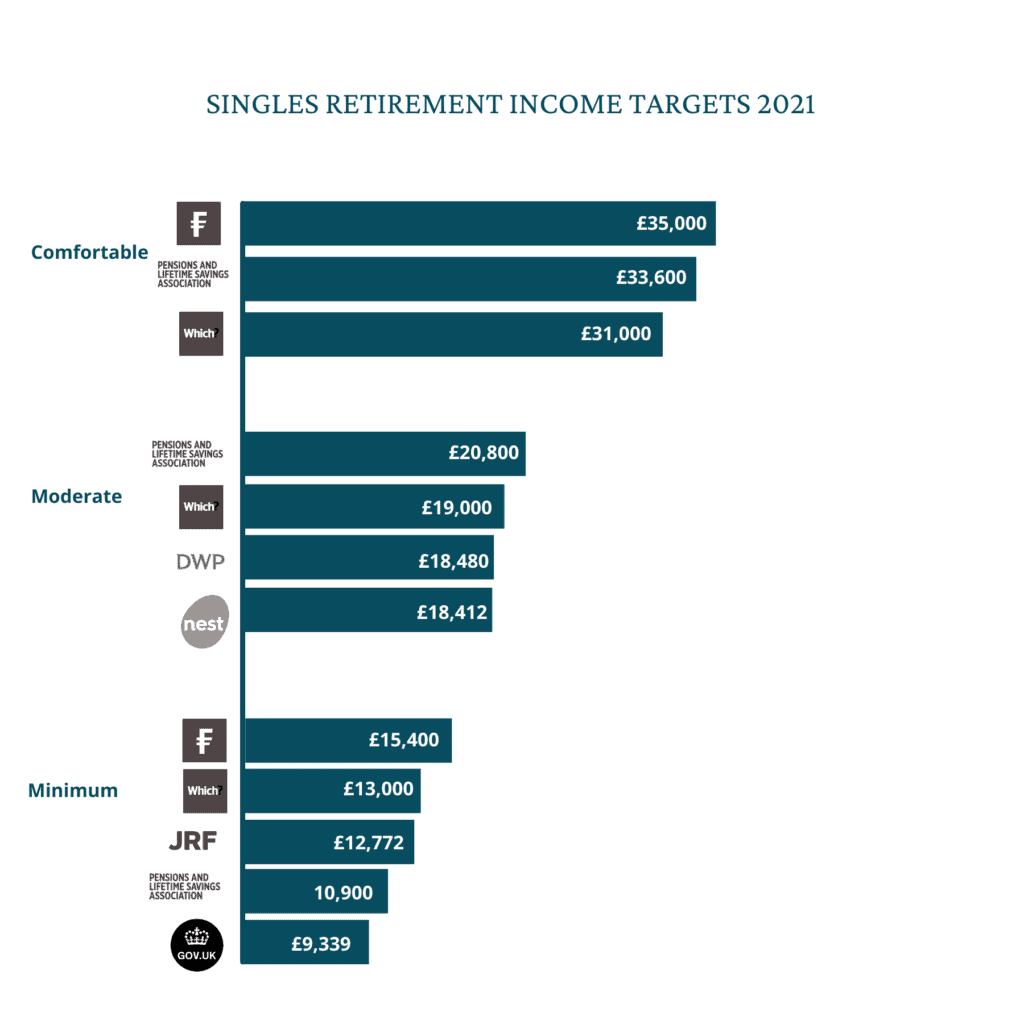

However another estimate by Tilney says you need £26,500 per year for a comfortable retirement. Royal London says, £17,500. The Department for Work and Pensions says you only need £16,817.

In reality. Experts can’t agree. Either on what constitutes a ‘good’ retirement income for a single person (estimates vary between £10.2K to £35K per year) or what ‘comfortable’ retirement even means.

It’s important to remember that these are averages and estimates, and may not include for expenses, which you might consider essential.

You are an individual.

When working out how much you need to comfortably retire as a single person our advice is that you consider yourself just that. A single person. An individual. Unique. With retirement needs unlike anyone else.

Simon Garber, owner of 2020 Financial and a retirement specialist with over 16 years experience says “We have customers who only need £10,000 per year in retirement. Others who want £100,000”.

“Equally, We have customers who never really want to stop working. Others who can’t wait for full retirement. Some have dependents and mortgages that will run well into their retirement years. Some are debt and dependent-free.”

Everyone’s circumstances are different.

In truth, Simon Says “your lifestyle should be the most important factor when starting to calculate how much you need to retire”.

It’s about lifestyle.

What do you like to do? How do you like to live? What does your ideal retirement look like? These are the things that should form the basis of your planning. You can’t rely on someone else’s research or pension calculator to determine the things you are then able to afford in your retirement.

Start thinking about your lifestyle now to help you start planning for the future.

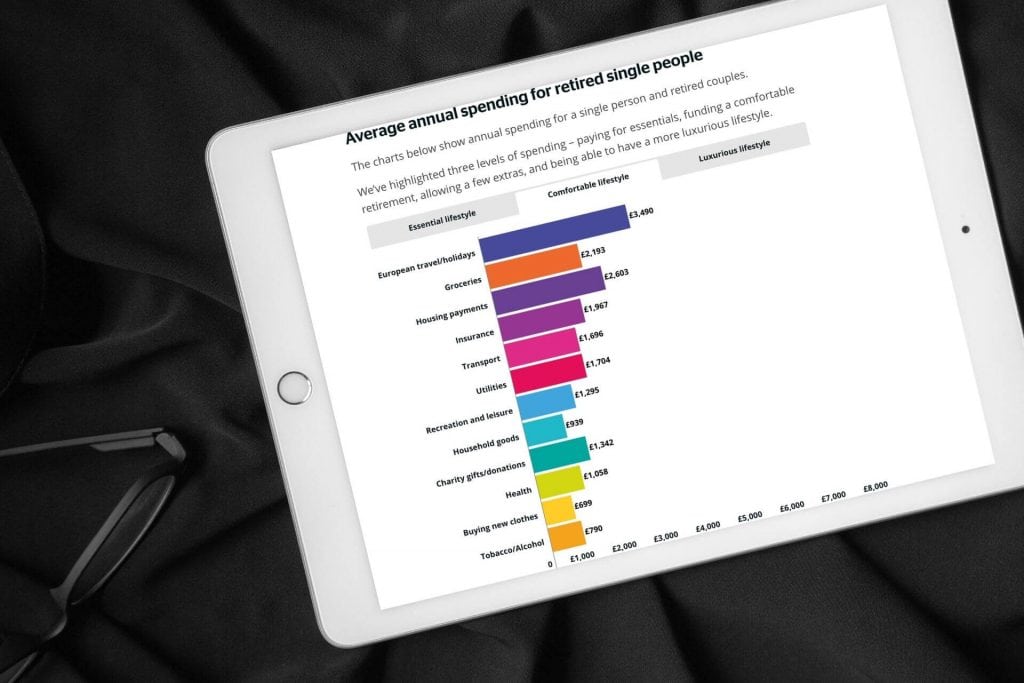

Which? says that a comfortable retirement for a single person costs around £20,000 per year. If you budgeted for this, it would include such things as:

- European Travel/holidays (£3,490 per year)

- Buying new clothes (£699 year)

- Recreation/Leisure (£1,295 year)

It also assumes you have paid off your mortgage. That you are dependent-free (or that your kids have flown the nest). But it doesn’t factor things in such as:

- Pets – an important fixture in many of our lives. The average cost of having a pet dog comes in at around £2750 per year.

- Christmas – The typical British household will spend an average £800 extra at Christmas on top of their normal monthly expenditure. It’s an annual expense that needs to be considered in your planning.

- And no matter what your age, cars need fixing, home improvements are still made, and domestic appliances and computers have a shelf life.

Beware of the research – The Which? Retirement Cost estimates

When calculating the cost of your single-person retirement income, online tools and research aren’t always your friend.

If we use the Which? research (quoted in this article) as an example. It was based on interviews with just 6,000 people. That’s 6,000 Which? members. A very narrow cross-section of society.

The research pool also consisted of both retired AND semi-retired people. And since Semi-retired generally spend less money on leisure, a figure that then increases in full retirement, this could skew their results.

There are lots of ways in which your retirement costs and needs might vary wildly from those interviewed – You might live in a different part of the country than those questioned, with higher or lower living costs. Or your lifestyle and spending habits could be very different.

Retirement planning is the biggest investment you are ever likely to make. Which is why we always recommend working with a professional.

That said, there are a few easy things you can do, to start to calculate your own personal retirement needs.

Estimate your retirement needs with Target Replacement Rate

There are lots of different ways you can make a good guess at your retirement income needs. One is Target Replacement Rate which works out the amount of money you will need in retirement to maintain your pre-retirement living standards.

This is based on the assumption that retired individuals generally spend a bit more on leisure and travel, a bit less on commuting, supporting children and mortgage costs etc.

So if your pre-retirement income was £90,000 per year. You should aim for a retirement income of around £63,000 per year.

As a general rule, your Replacement Rate figure would be around 70% of your pre-retirement income. This is also sometimes known as The two-third’s Rule – the goal of having around two-thirds’s of your pre-retirement income.

The Target Replacement Rate gives you a quick, albeit crude, way to estimate your retirement needs. However, it’s important to note that this figure is based on the assumption that you will have paid off your mortgage by the time that you retire.

And a report commissioned by Royal London actually estimated that around one-third of retirees may eventually end up renting. These costs can amount to around £6,554 a year (with UK rental prices rising every year for the last 10 years, and due to rise a further 15% by 2023). So unplanned rental costs could seriously compromise your retirement fund.

If you are renting or will still have a mortgage it’s important you factor in these additional costs.

How much does a single person need to retire at 55?

The younger you retire… the longer you’ll be living off your retirement fund.

The Pension Freedoms announced in 2014, allow you to access your private, defined contribution pension from the age of 55. The new rules allowed greater flexibility for how much you could take and how you were able to take it and gave people access to 25% of their pension as tax-free cash.

Obviously, in light of the new rules, there has been a greater uptake of those seeking to retire at 55. With people living well into their 80s and beyond, early retirement poses a particular challenge depending on your single person retirement pension needs.

When calculating how much a single person needs to retire at 55 there are many things to consider.

Living Longer

The average life expectancy for a woman is 89, and for a man, 86. If you retire at 55, that means your retirement fund needs to last around 15 years longer than someone who retires in their late 60’s. Many online retirement calculators assume people are retiring at 65. That could be 10 years of expenses not budgeted for!

Higher Outgoings

Your financial outgoings will fluctuate during your retirement years. The younger you retire, the more likely you are to still have higher outgoings. Mortgages may still need to be paid off. Children may still be in education.

Still active

Retiring younger also means you should be more physically active. There is much out there to enjoy! You could end up spending more money in earlier retirement on things while you are still active enough to enjoy them. Safaris and skiing spring to mind! But it may be global adventures or a variety of more active pursuits.

Most retirement calculators don’t take these things into consideration. So it’s important you factor them in. These outgoings will tail off as you progress through your retirement. But then other costs can begin to increase, such as the cost of care or medical costs.

State Pension

At 55, you will not yet qualify for your state pension. But the state pension is sometimes factored into online pension calculators. The state pension for a single person equates to around £160.18 per week for a man (£8,329 a year) and £152.55 per week for a woman (£7,933). If your retirement budget includes it, you will already be down around £8,000 per year for the first 10 years of your retirement.

That’s a big miscalculation!

How much does a single person need to retire at 60?

Everything that might impact a 55-year-old could also impact how much a single person needs to retire at 60, although helping older children through University might now be a case of helping them on the property ladder or assisting grown children financially.

No State Pension

At 60 you would still not qualify for state pension. So it’s important you don’t factor it in at this point. Which?, for example, includes the state pension in its retirement savings calculator. So when using online tools make sure you read their small print. Otherwise you could end up with a hefty shortfall in your planning.

Embrace the complex

Retirement planning for any age is complex. Your retirement will not fit into any standardised box. That said, what we know for sure, is that your lifestyle should always be the most important factor when starting to calculate how much you need to retire.

Working with a professional will help you create your ideal retirement lifestyle AND plan for life’s unexpected expenses.

How much does a single person need to retire at 66?

When you reach the current UK state pension age at 66, if you’re eligible, you’ll start receiving your state pension. It’s usually assumed that you’ll have paid off your mortgage, so ‘in theory’ you should have more income and fewer outgoings to fund from a private pension.

If you want to calculate how much you might need to retire at 66 then there is an abundance of retirement calculators for you. Most factor in receipt of a full state pension, which you may now (or nearly) be eligible for.

- They tend to assume you have paid off your mortgage.

- That any kids are now financially independent.

But that’s about as personalised as they get.

How much you need to retire at 66 rather than 55, 60 or even 70 is still entirely dependent on your outgoings and the type of lifestyle you intend to live.

In truth many people have mortgages that run into their 70’s. Kids return home. Grandkids arrive. And The Bank of Mum & Dad is still one of the UK’s biggest lenders.

In actual fact, regardless of how simple the budgeting may appear in the research, there are all manner of other larger costs that can frequently appear, and unexpectedly, but are a necessity.

Which is why it’s time to get personal.

Getting personalised retirement advice

If you’re single, you don’t have the retirement safety net of a partner’s pension, savings or assets, so it’s all the more important that you ensure your financial security for retirement whilst you still have the ability to plan ahead.

If you’d like to create a solid retirement plan, schedule a free, no-obligation call to discuss our retirement planning services.

{kind=link}