Schedule a free discovery call with a Financial Advisor

Use our ONS UK Life Expectancy Calculator to see how long you are likely to live, and how long your pension might need to last you in retirement

We’ve partnered with the Office for National Statistics to bring you their UK Life Expectancy Calculator. You can use this calculator to see what your life expectancy is based on your age, gender and national averages. You can also see what chance there is that you might live past 100.

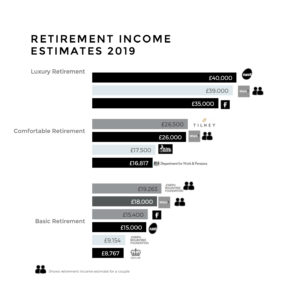

Exactly how much money you’ll need to enjoy a comfortable retirement depends mainly on two things:

- The length of your retirement and

- Your income expectations

how much will I need

Life Expectancy Calculator

The length of your retirement will depend on when you retire and how long you live. The earlier you retire the longer your retirement is likely to be. None of us knows how long we’re going to live, so knowing how long your pension will need to last is like asking ‘how long is a piece of string?’, which makes retirement planning a bit tricky. Since none of us has a crystal ball, it’s not an exact science, but, we can use average life expectancy as a best guess to inform our retirement decisions and plan accordingly.

Being more informed about how much longer you potentially have to live is no bad thing, especially when it comes to financial planning. People are living longer and needing to fund longer retirements. On average, people in the UK aged 55 today will live to their mid-to-late 80s. Around 1 in 10 men and 1 in 5 women this age will live to 100 – and receive their telegram from The Queen.

1. Life expectancy is calculated using the 2014-based principal projection for 2016 in the UK produced by the ONS.

2. Your state pension age as of 1st January depends on your particular date of birth.

How long are you likely to live?

Enter your details and sex at birth to find out your life expectancy, your chance of living to 100… and how long you’ll likely need to make your pension pot last.

What's my life expectancy?

Enter your details in our calculator and find out your life expectancy, your chance of living to 100… and how long you’ll likely need to make your pension pot last.

Why life expectancy matters for retirement planning

Long-term forecasting

Although life expectancy isn't a crystal ball, and none of us knows how long we might live. Life expectancy is still a useful tool for long-term forecasting & planning. Especially if you have a family history of longevity

Retirement age planning

Life expectancy and longevity can help you make more informed decisions about when you might like to retire and if you have enough money saved for retirement.

Pension POT BUILDING

Understanding your life expectancy can help you understand how much you might need in your pension pot and save and plan accordingly.

Download our free expert guide to

Planning for your retirement

Discover everything you need to know about retirement planning in our expert guide

Frequently Asked Questions

Retirement planning doesn't have to be complicated, with the right plan in place, and the right support, your dream retirement can feel like a breeze.

We've laid out some simple steps in retirement planning below, but if you get stuck, just reach out and one of our retirement planning specialists will be happy to help you:

- Decide what type of retirement you want to enjoy

- Set a retirement date

- Work out a retirement budget based on what feels like a good retirement income for you.

- Request a pension forecast - request your state pension forecast here https://www.gov.uk/check-state-pension

- Get your pension estimates - track down old pensions with the Pension Tracing Service (0800 731 0193)

- Talk to a Financial Advisor to create a retirement plan, work out how you will pay down any debt and if it's worth consolidating any old pensions

- Put your retirement plan in action and look forward to enjoying your retirement.

- Don't forget to periodically review your plans every year to make sure you're on track, because circumstances can change and the earlier you respond the more time you have to course correct.

Speak to a Financial Advisor

No commitment, no hard sales, just a quick chat with one of our pension transfer specialist to see if we can help

NOTE:

This life expectancy calculator is provided for general information purposes only.

Any information contained within this website should not be deemed to constitute financial advice, and should not be relied upon as the basis for a decision to enter into a transaction, or as the basis for any financial or investment decision. It is provided for general information and it is vital (and in most cases a regulatory requirement) that you contact a Financial Adviser for tailored professional advice in regard to pension and retirement planning.

- No individual or company should act upon such information without receiving appropriate professional advice after a thorough examination of their particular situation. We cannot accept responsibility for any loss as a result of acts or omissions taken in respect of any articles.

- If you are a member of a pension scheme with safeguarded benefits, it is likely it would be in your best interests to retain the safeguarded benefits.

- Make sure you understand all the risks before investing.

- The value of investments and the income they produce can fall as well as rise and you may not get back your original investment. Past performance is not a reliable indicator of future results.

Don't miss

Our most popular posts

These are some of our most popular posts. Click below or head over to our blog to see other helpful articles on pensions, retirement and investing.