If you’re planning on taking a lump sum from your pension, it is important to understand the tax implications of doing so, especially if you’re accessing your pension at 55 and still working, as a higher rate taxpayer you could end up paying 40% tax on any lump sum you withdraw from your pension pot.

We’ve selected 5 of the best Pension Lump Sum Tax Calculators we’ve found to help you with your planning, but before we share them, here’s some important information:

How much tax will I pay on my pension lump sum?

The amount of tax you’ll pay on any pension lump sum will depend on whether or not you’ve used your 25% tax-free pension allowance, what your current income level is and whether your pension lump sum pushes you into a higher tax bracket.

It’s important to remember that anything you draw down from your pension will be seen as taxable income in the eyes of the taxman. That means it can very quickly move you into a higher tax bracket. That’s why it is crucial that you understand your unique tax implications so that you don’t end up losing more money than you are prepared for.

A pension lump sum calculator is a great way to get a ballpark figure for your tax implications: however, these should only be viewed as an initial idea and should never replace professional advice. Professional advice will often save you money in the long run as it takes into account your personal circumstances and goals for the future, utlising your investments and maximising their return.

To get things started, you can use the calculators below to give you an idea of how much tax you’ll pay on your pension lump sum.

What rate of tax do I pay on my pension?

Pensioners are subject to the same income tax rules as those of working age in the UK. As a pensioner, both state and private pensions are counted as taxable income.

You therefore need to figure out the rate of tax that you will be liable to pay on your pension. This can result in a serious dent in your retirement fund. The moment you take your investment out of a pension pot, it loses all of the tax-efficient benefits that it has been soaking up. Not only will it stop accumulating as much, but it will also start to lose value. For starters, if you take out over 25% of your drawdown pension, it will be taxed at your highest amount. The investment that you cash in will be added to your overall income: once you pass £50,271, this could result in your landing in the highest rate tax bracket… A massive 40%.

Plus, if you plan to put your investment into your bank account, you will experience limited interest rates; especially in comparison to the benefits available with a pension investment. We explain this (and much more) in finer detail on our Pension Drawdown Advice page. Even as a pensioner, you could find yourself on a hamster wheel of tax implications… Taxed for taking the money out in the first place, and then taxed on any money earned.

The table below shows the tax rates you pay in each band if you have a standard Personal Allowance of £12,570.

(Please note: Income tax bands are different if you live in Scotland.)

Income tax bands are different if you live in Scotland.

| Band | Taxable income | Tax rate |

| Personal Allowance | Up to £12,570 | 0% |

| Basic rate | £12,571 to £50,270 | 20% |

| Higher rate | £50,271 to £150,000 | 40% |

| Additional rate | over £150,000 | 45% |

You can also see the rates and bands without the Personal Allowance. Keep in mind that you do not get a Personal Allowance on taxable income over £125,140.

Let’s put it into context: the current state pension is £179.60 a week which tallies up as £9339.20 a year. Assuming you’re eligible for the full state pension, you can earn a further £3230.80 income from different sources before you start paying tax: for example, your personal pension, workplace pension, rental income, salary and savings accounts.

In addition, if you’re married there may be ways for you to utilise your spouse’s personal allowance to offset your own tax liability (and lower your tax rate). Saying that, tax rules are complicated (and can result in hefty fines!) so we strongly encourage you to speak to your accountant before relying on this.

Pension Lump Sum Tax Calulators

There’s no substitute for tailored, professional advice, especially when it comes to your finances and tax, it pays to be properly informed. But these Pension lump sum tax calculators can be a good place to start your pension and tax planning.

Remember, these calculators provide a guide and should not replace professional advice. Professional advice will often save you money in the long run, always talk to a Financial Adviser and/or your accountant first.

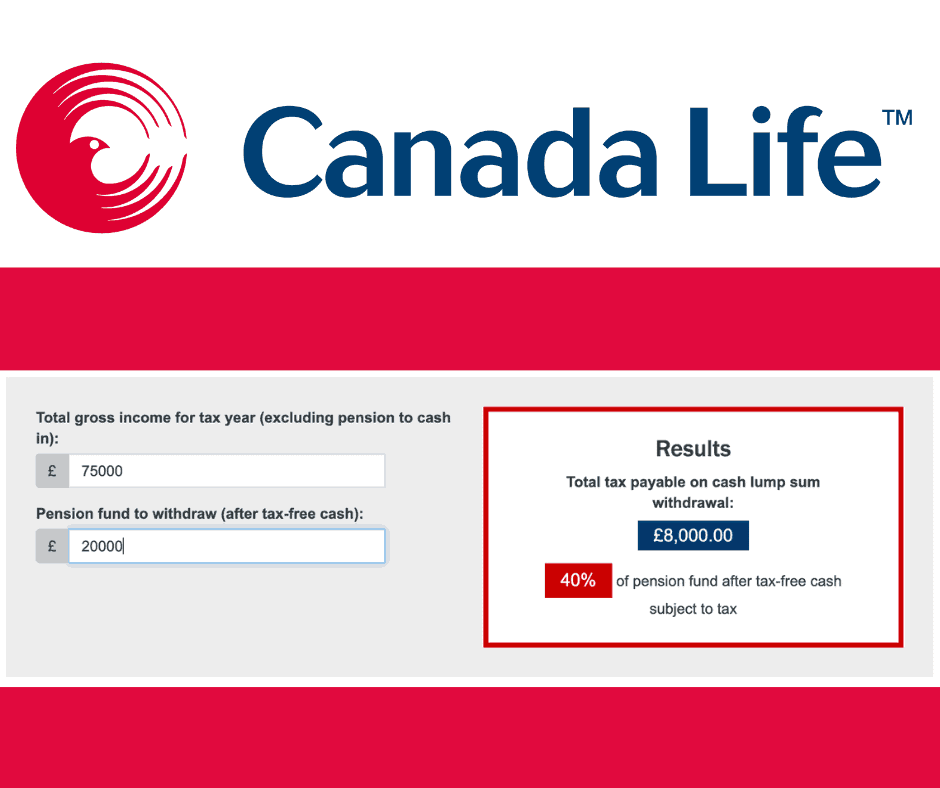

1) Canada Life

The simplest calculator that shows you how much tax you might pay on any pension withdrawals after you’ve taken your tax-free cash.

https://www.canadalife.co.uk/tools/pension-tax-calculator

2) Hargreaves Lansdown

This calculator provides you with an indication of the tax you may have to pay based on current rates and allowances. It takes into account personal tax allowances. It also gives the option to work out Scottish income tax levels.

https://www.hl.co.uk/retirement/preparing/tax-matters/income-calculator

3) Aviva

The Aviva Pension Withdrawal Tax Calculator is the most comprehensive of the 5 we tested, as it lets you choose how to take your tax-free cash on lump sum withdrawals from your pension pot. You can opt to take all of your tax-free cash first, take 25% of each withdrawal as tax-free cash or specify the amount of tax-free cash you would like to take.

https://www.direct.aviva.co.uk/myfuture/PensionWithdrawalTaxCalculator

4) Which?

Consumer champion Which? have created their own Pension Lump Sum Tax Calculator. This calculator will help you figure out how much income tax you’ll pay on a lump sum after you’ve taken your 25% tax-free cash.

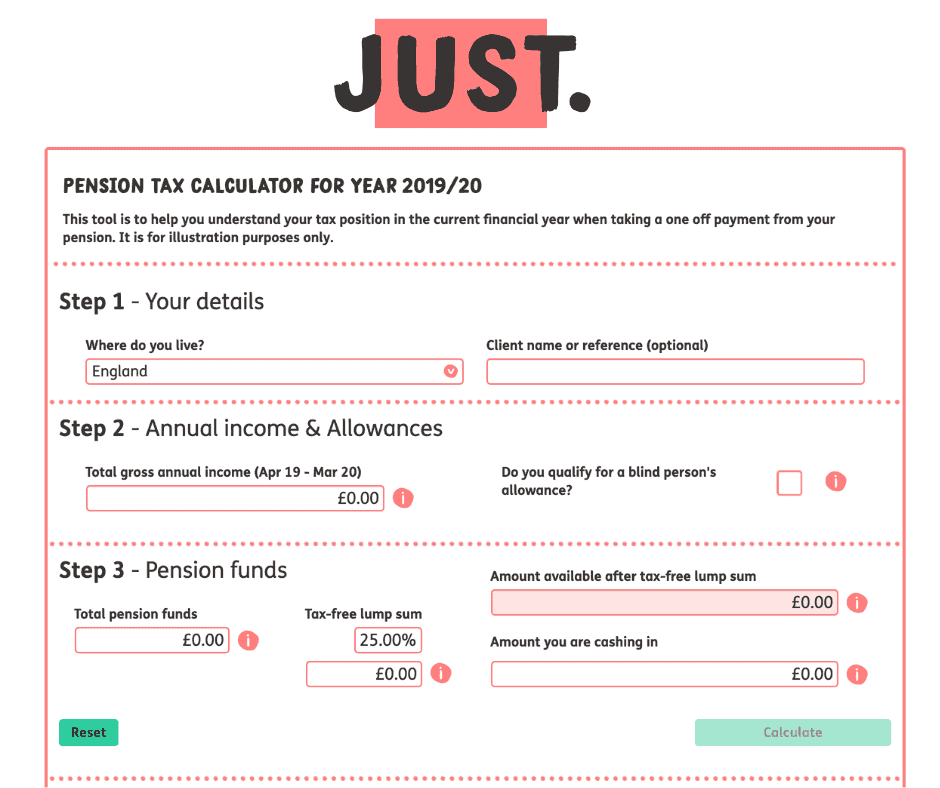

5) Just Adviser

Lets you choose your taxation based on where you live in the UK. You can select to take some or all of your tax-free cash and it will work out the tax due on anything over that. Technically, this is a tool for financial advisers to use, but you can access the website as a consumer.

https://www.justadviser.com/financial-planning/calculators/pension-taxation/

Can I claim tax back on a pension lump sum?

Be aware that when you first access your pension or take a lump sum from your pension you may be given an Emergency tax code. If this happens you may pay more tax than required.

While this can come as a shock, it is possible to claim tax back on a pension lump sum if you’ve overpaid. You will need to contact HMRC directly and request the tax return through them. You can find out more information on the process here.

HMRC are usually pretty good at processing tax rebates if they’ve taken too much tax from your pension withdrawals but it won’t be instantaneous, so if you’re withdrawing money for something time-sensitive, plan ahead of time and don’t leave it too late.

If you want to avoid overpaying tax on your pension lump sum it can be helpful to speak to your accountant and plan ahead to make sure you don’t get put on the wrong tax code.

Can I take tax-free cash from my pension and leave the rest?

With the introduction of Pension Freedoms in 2015. You can now take your entire pension pot in one go once you reach 55. Of course, anything that you drawdown over 25% will be charged at your highest tax bracket; since your pension income counts as taxable income, this could push you through to a pricier tax band.

If you choose to, you can therefore take your tax-free cash and leave the rest. But, before you do so, consider the fact that it will reduce the amount you have invested in your pension pot, so there will be far less money in your investments and you will have less to last you through retirement. Depending on the type of retirement you hope for in your golden years, this could throw a real spanner in the works.

Our advice is that if you don’t have an immediate need for the money, you may be better off leaving it invested in your pension: it is the most tax efficient container you’ll ever get. Keep in mind that if you opt to take your pension lump sum and leave it in cash or put it in a standard savings account, your money will likely be eroded by inflation. Talk to your financial advisor about ring-fencing money in a low-risk investment if you’re worried about risk.

Another thing to take into account is that pensions sit outside your estate and therefore aren’t subject to inheritance tax like the rest of your assets. However, any money you take out of your pension immediately becomes part of your estate and liable for inheritance tax at 40%.

Learn more about Inheritance Tax Rules

So, before signing on the dotted line, ask yourself:

- Will it affect you being able to continue to pay into your pension?

- How will you fund your retirement?

- Will it affect inheritance tax for your loved ones if you die?

RELATED: PENSION LUMP SUM | A COMPLETE GUIDE

How can I avoid paying tax on my pension UK?

There are several legitimate ways to avoid paying tax on your pension (without stepping into tax avoidance territory). The main ways are maximising your use of your 25% tax-free cash and taking full advantage of your personal allowance.

Current rules allow you to take 25% of your pension tax-free. This can be taken as a lump sum or as drawdown income. You can do this from the moment you hit 55 (57 from 6 April 2028), and is one way to take advantage of a tax-free cash chunk.

Another way is to make use of your personal tax allowance. As of 2021, the personal tax allowance is £12,570 a year and this can be used to strategically (and 100% legally) minimise your tax bill. For example, you may consider blending your tax-free cash from your pension with your income in order to reduce your tax liability. If this does sound like the route for you, we recommend you speak to both your accountant and a financial advisor: it’s can be a tricky process, and one you don’t want to get wrong. For more information, read our blog How can I avoid paying tax on my pension UK?

Tax Planning for Retirement

It’s important to understand that effective retirement planning could reduce the amount of tax you need to pay, by optimising the way you take your tax-free cash, especially if you’re still working. Remember, you don’t have to take your tax-free cash at 55 and you don’t have to take it all in one lump sum. Find out more about your options here.

Read more: Can I take my pension at 55 and still work?

Personal Allowance and Lump sum withdrawal

It’s important to understand that all of these calculators assume the full personal allowance and tax bands are available, but depending on when you take your lump sum, they may not be.

For instance, in April, the first month of the tax year, only 1/12th of your personal allowance and tax bands are available so you may pay a disproportionate amount of tax on your withdrawal, which you will need to reclaim from HMRC.

Tax-Free Cash and Inheritance Tax

If your estate is over the Inheritance Tax Threshold It’s important to know that once you withdraw your tax-free cash from your pension, it immediately becomes part of your estate and therefore liable for inheritance tax at 40%. Any money – including tax-free cash held within your pension is not usually liable for inheritance tax.

Looking for more tools to help you plan your retirement? Head over to our Pension Calculator page and find our collection of useful calculators for retirement planning.

{kind=link}