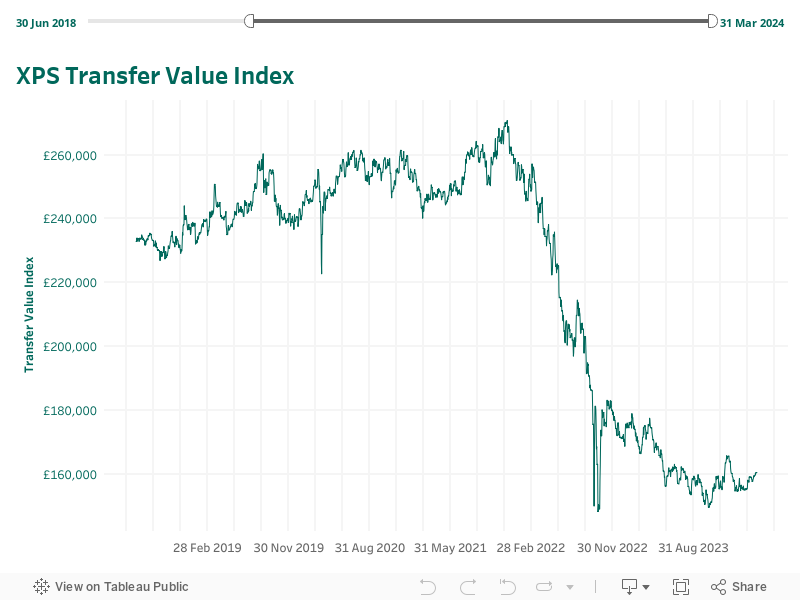

March 2023, saw defined benefit pension transfer values fall to their lowest month-end level since 2016, far below the record highs we saw in December 2021. And despite some small positive fluctuations, there’s no immediate sign of recovery, with transfer values continuing to fall in the second quarter of 2023.

Whilst many factors affect defined benefit pension transfer values, the climbing interest rate is the main factor driving the sudden fall in transfer values in 2023.

The ultra-low interest rates fuelling soaring UK transfer values from 2018 to 2021 have now gone. After sitting at 0.1% for much of 2021, the Bank of England has conducted a number of Interest rate rises. UK interest rates now sit at a 15-year high as the Bank of England attempts to reduce stubborn inflation which remains well above the UK target inflation rate.

The rising interest rates, coupled with other market pressures (both global and in the UK) have affected transfer values, and we have seen massive falls across the board.

CETV values 2023

Cash equivalent Transfer have continued to fall throughout 2023. From record highs in December 2021, CETV values saw new record lows in March 2023, and although there’s been some recovery, we’re nowhere near the values we saw at the end of 2021.

In June 2023, the XPS pension transfer value index puts the estimated cash transfer value of a 64-year-old member with a pension of £10,000 a year at £162,000, down from £258,926 on 1st Jan 2022.

The falling transfer values appear to be affecting people across the board, although with Interest rates hitting 15-year highs in Aug 2023 despite falling inflation, there is a hope that the future may bring better news for those wanting to transfer their DB pension.

What factors affect pension transfer values

According to consultancy firm LCP, two key factors affecting pension transfer values are

- The ‘generosity’ of the scheme – if schemes are de-risking their investments, they are more likely to offer a higher value; and

- Members’ longevity predictions – the longer its members live, the more costly the scheme is to run and transfer values tend to be more generous.

It could be that the long-term impact on life expectancy due to the covid-19 pandemic and related health crises could also play a part in reducing transfer values, although, in the UK, this is expected to be reversed in the coming years.

Several other factors can also affect pension transfer values both positively and negatively, including:

- Interest rates

- Inflation levels

- Gilt yields & stock market activity

- Member’s age in relation to scheme retirement age and

- Scheme funding position

Read more: What’s a good CETV?

Do transfer values increase with age?

It’s worth noting that pension transfer values tend to increase closer to your scheme’s retirement age.

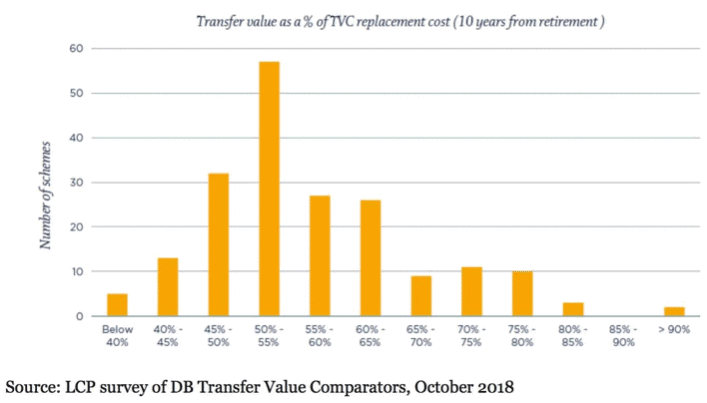

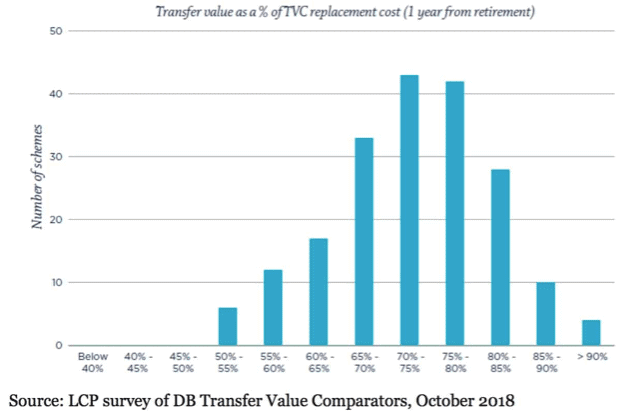

Research published by Royal London and LCP has shown that the relative value of transfer values tend to rise the closer members are to retirement.

The graphs below show that on average those 10 years away from retirement are more likely to have transfer values with a lower comparative value than those closer to retirement. I.e. the closer you are to retirement, the closer your transfer value will be to the true market value of your pension.

Typically, the guidance is to avoid transferring out of your scheme and to stay put if your retirement is still a long way off. If you’re under the age of 50 it’s generally not advisable to consider a transfer as the risks and costs involved can be prohibitive.

Of course, age isn’t the only factor affecting transfer values so it’s not a guarantee of a higher transfer value. It’s worth speaking to a qualified pension transfer specialist for tailored advice. Pension transfer isn’t a one-size fits all affair.

Why are CETVs falling?

CETVs reached record levels in December 2021, but the extreme inflationary pressures and global stock market volatility paired with rapid interest rate rises have seen CETVs fall steeply to record lows in 2023.

Pension trustees manage pension funds and guarantee members’ pension income (adjusted for inflation) for life. UK inflation rates hit a 40 year high in 2022 and remain stubbornly above the 2% target set by the Bank of England, pushing up the cost of providing pensions.

Whilst transfer values should offer a fair representation of value, Pension trustees’ first priority is securing the health of the pension scheme for its active members. As scheme costs rise, it makes sense that they would seek to discourage people from transferring out by offering falling CETVs.

Advice for people considering a transfer

Pension Transfer Specialist Simon Garber says – “Most people I speak to have the luxury of time, they don’t need to make an immediate decision. Markets are cyclical, we might be experiencing a painful economic time now, but it won’t last forever.”

He reminds people

“if your CETV has fallen, it’s only your transfer value that has fallen; the value of your pension hasn’t fallen at all. In fact, your pension is adjusted for inflation, so all the time you’re in the scheme, the value of your pension is increasing even if your transfer value isn’t. If you opt to transfer now, you might crystalise a loss that you could otherwise avoid by being patient.”

Don’t make a panicked decision to transfer based on the fear your transfer value may fall further still in the future. If you’re concerned about your options, the best advice is to seek professional advice from a Qualified Pension Transfer Specialist.

Speak to a Pension Transfer Specialist

We offer a free, no-obligation introductory call with our Pension Transfer Specialist, they can signpost you to useful information and explain our pension transfer process. Book your free call today.

{kind=link}