If you’re planning your retirement, you might have heard of the pension freedoms that allow you to access a tax-free lump sum from your pension at 55. But did you know that taking a pension lump sum is just one of the ways that you can now access your pension:

Your pension options at 55:

- Leave your pension invested if you don’t need to take money straight away

- Take the tax-free cash and leave the rest invested

- Take some or all of the money as a cash lump sum

- Buy an annuity to provide a lifetime’s secure income

- Use a combination of the above

If you’re considering taking a pension lump sum, it’s worth understanding how they work, the rules, and whether it’s in your best interest. We’ve answered some of the questions we get asked most frequently below, but please get in touch if you have any other questions, and we’ll be happy to help.

What is a Pension Lump Sum?

A Pension lump sum is a lump sum amount taken from your pension. How and when you can take it depends on the type of pension scheme you have.

Taking a pension lump sum from a Defined Contribution pension

If you have any pension where you build up a pension pot that you will use to provide you with an income in retirement – it’s known as a Defined Contribution Pension.

Personal pensions, SIPPs and standard workplace pensions are all types of Defined Contribution Pensions. If you have a Defined Contribution Pension, you will typically be able to access a cash lump sum from your pension from the age of 55.

- Taking a pension lump sum from a Defined Benefit/Final Salary pension

Defined benefit schemes guarantee to pay you a set amount every year in retirement (usually adjusted for inflation every year).

Some defined benefit pension schemes automatically offer their members a cash lump sum in addition to the pension you’ve built up, which you’ll typically get when you retire.

In other defined benefit schemes, you may be able to exchange some of the pension you’ve built up for a cash lump sum (known as commutation – see how it works here). With commutation, you get a lump sum upfront (typically when you retire), but you get a smaller pension every year.

- Pension Lump Sum – Defined Contribution vs Defined Benefit

Most of the flexibility to access lump sums from your pension applies exclusively to those with a defined contribution pension (also known as a money purchase pension). If you have a defined benefit/final salary pension, you’ll need to check with your pension trustees for the rules that apply to your scheme. Find out how the pension rules affect Final Salary Pensions.

Can I take my pension as a lump sum?

With the introduction of Pension Freedoms in 2015. You can now take your entire pension pot in one go once you reach 55. That said, there are several things you should consider before you do so, and you should seek professional advice first

Things to consider:

- How much tax you’ll pay

- Will it affect your ability to continue to pay into your pension?

- How will you fund your retirement?

- Will it affect inheritance tax for your loved ones if you die?

Should I take a lump sum from my pension?

If you opt to take a lump sum from your defined contribution pension, it will reduce the amount you have invested in your pension pot, so there’s less money in your investments, and you will have less to last you through retirement.

If you don’t have an immediate need for the money, you may be better off leaving it invested in your pension. If you opt to take your pension lump sum and leave it in cash or put it in a standard savings account, inflation will likely erode your money. Talk to your financial advisor about ring-fencing cash in a low-risk investment if you’re worried about risk.

Another thing you should be aware of, especially if you’re concerned about inheritance tax, is that pensions sit outside your estate and therefore aren’t subject to inheritance tax like the rest of your assets. However, any money you take out of your pension immediately becomes part of your estate and is liable for inheritance tax at 40%.

Learn more about Inheritance Tax Rules

How much tax will I pay?

The first 25% of your pension is tax-free; after that, you’ll pay tax at your highest marginal rate.

However, you may end up paying emergency tax, in which case you will need to reclaim the overpaid tax directly from HMRC. You may also find that your total tax allowance is not yet available, especially if you opt to take your lump sum at the start of the tax year; again, if you overpay tax, you can reclaim it.

Your pension trustees will usually work with the tax code that HMRC give them. Unfortunately, it’s not uncommon for this to be incorrect, and you could over or underpay tax in the early months of taking a regular income from your pension. The good news is that HMRC usually is pretty good at sorting out any issues if you call them.

Using these Pension lump sum tax calculators, you can find out how much tax you’re likely to pay on your lump-sum.

Is a pension lump sum classed as income?

The first 25% you take from your pension is tax-free, but anything after that is classed as income. How you’ll be taxed depends on how you opt to take your pension lump sum – there are several ways that you can do so:

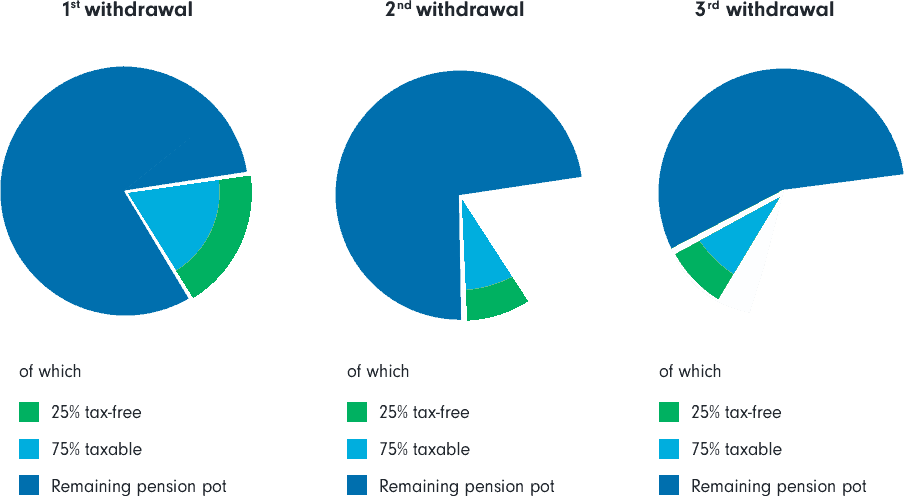

With the pension freedoms of 2015, you can now take your pension as a series of cash lump sums if you have a defined contribution pension. The first 25% will be tax-free, taxing the rest at your marginal rate.

You can start taking chunks of cash from your pension pot from 55. you may even use lump sums from your pension to fund early retirement or use the money to subsidise phased or semi-retirement. You could also use Flexi-access drawdown, with the freedom to take as much or as little from your pension as you need.

If your pension is invested, it’s worth remembering that the value of your remaining pension pot can go down as well as up, so the amount available to you in the future could change.

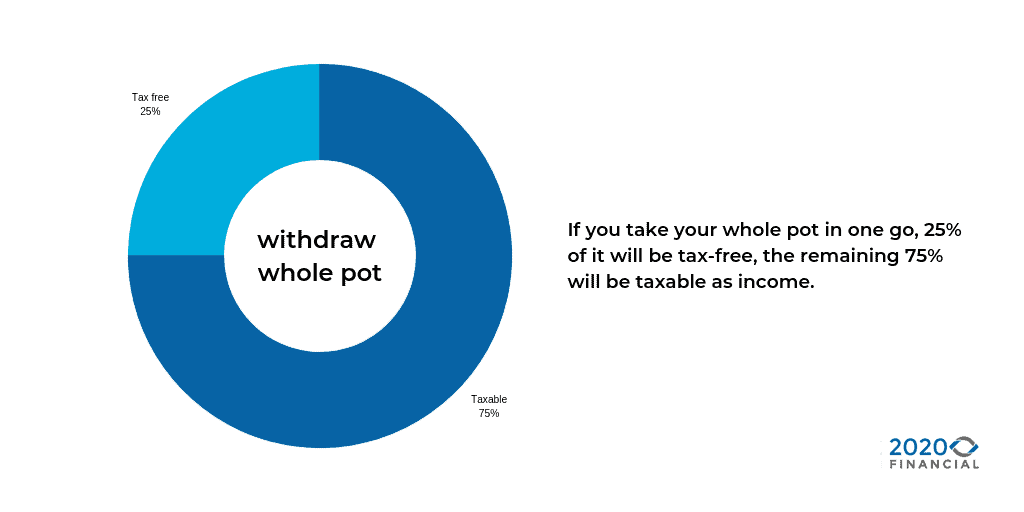

Take your whole pot as a lump sum – example.

You can also take your entire pension pot as one cash lump sum. 25% will be tax-free, but the rest of your pension pot will be taxed at your marginal tax rate. Depending on the size of your pension pot and your existing earnings – this could push you into a higher tax bracket.

Taking your Tax-free Lump Sum – example

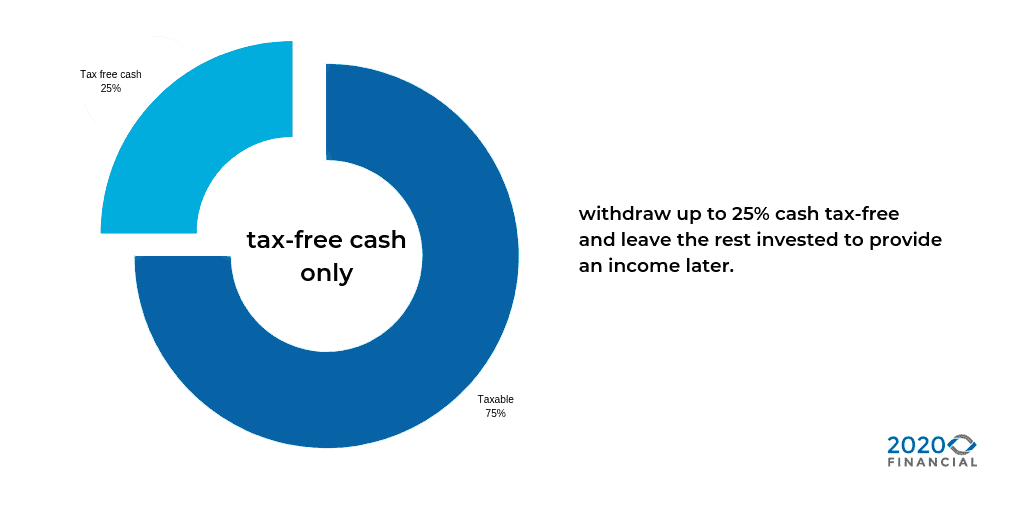

You can take your entire tax-free lump sum – 25% of your pension pot in one go, leaving the remaining 75% invested for your retirement.

It might be tempting to take all of your tax-free cash at 55, especially if you want to clear down debts, pay off a mortgage or buy an investment property. Still, you should carefully consider the impact of doing so on the size of your pension pot and whether it will leave you enough money for retirement.

You don’t have to take all of your tax-free cash in one go; you could take some now and leave the rest invested for later.

Can I take 25% of my pension tax-free every year?

You will only ever get to take 25% of the total value of your pension as tax-free cash. It is not an annual allowance.

If you access your pension pot at a series of lump sums known as FLUMPS or UFPLS, then the first 25% of any chunk you take will be tax-free, and the remaining 75% will be taxable at your marginal rate. If you take your money this way, you can access 25% of your pension tax-free every year, but it will only be 25% of the lump sum you take.

What’s a UFPLS

UFPLS or FLUMPS, as they are also known – stands for Uncrystallised Funds Pension Lump Sum. They are lumps of cash that you can take from your pension without converting it into a drawdown scheme.

How do I take my tax-free cash from my pension?

If you want to access a lump sum from your pension, you’ll need to contact your pension scheme directly.

If you want to access your pension flexibly through Pension drawdown,

- Find out if your current scheme offers a flexible access drawdown option; some older schemes don’t. If your scheme doesn’t provide pension drawdown, you’ll need to transfer your pension to a scheme that does.

- If your pension scheme allows Pension drawdown, then you’ll be asked to fill in some forms and provide proof of identity before any money is paid to you.

How long does it take to get my Pension Lump Sum?

Pensions are not like bank accounts; it can take a bit longer for pension trustees to process requests for lump-sum amounts. It’s not unusual for it to take 2 weeks or more for your pension company to get your money paid out to you.

If it’s the first time you’re requesting money from your pension, it could take even longer. Pension trustees aren’t known for their lightning-fast customer service, so plan and leave plenty of time until you need the money.

How many pensions can you cash in?

If you have several small pensions you may be able to take them as cash lump sums under the trivial lump sum rules as long as you are 55 or meet the criteria for ill-health early retirement. You can take up to 3 non-occupational pensions up to £10,000 each and an unlimited number of occupational pensions worth up to £30,000.

It’s worth noting that the same tax rules apply. The first 25% is tax-free; anything after that, you’ll pay tax on it.

Can I take Pension Lump Sum at 55?

Changes to the pension rules in 2015 mean that you now have much more choice about accessing your pension at 55. For example, if you have a defined contribution pension, you can access it from 55.

At 55, you can:

- Keep your pension invested and continue to pay into it, and receive tax relief until you are 75

- Access 25% of your pension pot as tax-free cash and leave the rest invested

- Take your entire pension pot as a cash lump sum

- Take just part of your pension pot as a cash lump sum

- Use some or all of your pension pot to buy an annuity to provide a lifetime’s secure income

- Use a combination of the above

Pension lump sum and the Money Purchase Annual Allowance

It’s worth noting that as soon as you start taking an income from your pension, you’ll trigger the Money Purchase Annual Allowance, which drastically reduces the amount you can pay into your Money Purchase Pension (also known as a Defined Contribution Pension).

Things that will trigger the MPAA:

- Taking your whole pension pot as a lump sum or taking ad-hoc lump sums

- Going into a Flexi-access drawdown scheme and taking an income

- Buying an investment-linked or flexible annuity where your income could go down

- Taking payments that exceed the cap on a pre-2015 capped drawdown plan

Read more about the Money Purchase Annual Allowance here

Final Salary Pension Lump Sum

The rules around Final Salary Pensions (Defined Benefit Pensions) are slightly different. Your scheme trustees set the rules about when and how much cash you can access from your pension as a lump sum. So you’ll need to check with your pension scheme directly.

You might automatically be offered a cash lump sum as well as your pension; this is normally true if you’re in a public sector defined benefit scheme. Usually, the lump sum is paid when you start taking your pension.

If you don’t automatically get a cash lump sum from your pension, it may be possible to swap some of your future pension for a lump sum now. This is called commutation and the amount you will have to swap is known as the commutation factor, which your pension scheme administrators decide.

It’s worth getting advice from a pension specialist if you’re trying to decide whether or not to take your pension early or whether you should commute your benefits to get a cash lump sum. It can be hard to understand the true value of the benefits you might be giving up – getting the right advice now could save you £££s in the future.

Need advice about your Pension Lump Sum?

If you need advice on how and whether to take your tax-free lump sum or if you need help moving your pension into a suitable drawdown scheme, we’d be happy to help. Schedule a free call with one of our Independent Pension Advisers today. You might also be interested in our new pension drawdown calculator (click here).

{kind=link}