It’s a question that we are asked time and time again: what is a good cash-equivalent transfer value? The answer isn’t a quick one – in fact, it depends on an enormous number of factors.

A good cash-equivalent transfer value (CETV) is one that gives you the funds and benefits needed that can be invested and will enable you to fulfil your personal goals for retirement.

While recent years have seen an influx of people transferring out of their final salary pension scheme – largely due to a spike in transfer rates – there are many things to consider before taking that leap of faith. For starters… Is your cash-equivalent transfer value as good as it looks on the surface?

There is no cookie-cutter answer. The ‘worth’ of your CETV will depend on your unique goals and needs.

CETV meaning

Your cash-equivalent transfer value is the amount your pension scheme will give you if you choose to transfer out of your Final Salary Pension Scheme. This is not the same as your pension fund amount.

All pension scheme providers will calculate transfer values differently; there is no ‘one size fits all’ approach to these calculations. Plus, very few schemes will publish their precise calculation method. However – as a starting point – they will calculate your CETV by identifying the cash amount needed to buy the final salary scheme benefits if invested on the day of the calculator.

This will be influenced by several factors, including:

- Age

- Retirement age

- The rules in place with the scheme provider

- How well the scheme provider is performing

- How much you plan to be paid every year in retirement

- Life expectancy

- Marital status

- The current cost of living

- Scheme investment costs and returns

Typically, you can expect an annual update from your pension scheme administrator detailing the necessary information; if not, you can ask for an up-to-date estimate of your CETV from your scheme provider.

What is a good Cash-equivalent transfer value?

How long is a piece of string?

One of the biggest sticking points we find when speaking to clients is that an initially impressive CETV figure may lead to you losing money and benefits. After all, if the investment doesn’t help you achieve your retirement goals, it simply isn’t doing the job.

We get it – it’s easy to get excited by seemingly endless zeros and a higher transfer value. And there’s no doubt that a higher CETV is going to feel far more attractive than a lower one. But, it’s crucial to remember that a high CETV does not necessarily mean a good one.

A good CETV gives you the opportunity to meet your lifestyle and financial goals during your retirement; to know whether it’s ticking the boxes, you need to take your personal circumstances into account. Our goals are different, so what makes a good CETV must be subjective.

How is a CETV calculated?

Your CETV is calculated by your pension scheme administrator, and this calculator takes several different components into account.

All scheme providers will calculate transfer values differently as there is no one set of rules that providers are required to follow. Their calculations will be based on the amount they deem fair to buy your final salary scheme benefits, and this will be influenced by:

- The estimated value of your pension at retirement

- Your age and how close you are to retirement

- The Investment Strategy of the scheme you are in and

- The position of the Financial markets when you request your transfer value

- Your Pension Schemes Health

You may be handed a seriously impressive transfer value… And you may feel pretty damn excited about it. We strongly encourage you to look at the pros and cons before you sign, seal, and deliver the transfer. Are you getting enough for all the benefits you will give away?

What is a good CETV multiple?

CETVs can range from anywhere between 20-25 times your pensionable income, although some schemes offer surprisingly generous transfer values and some far less. Regardless of whether the offer feels on the higher or lower end of the scale, be sure to check that you have been offered a fair transfer for the benefits that you are giving up.

Many factors come into play here. Although transfer values were at record levels in 2021, 2022 has seen a steep fall in transfer values. This is due to the many external influences (such as the market, interest rates and inflation) impacting rates.

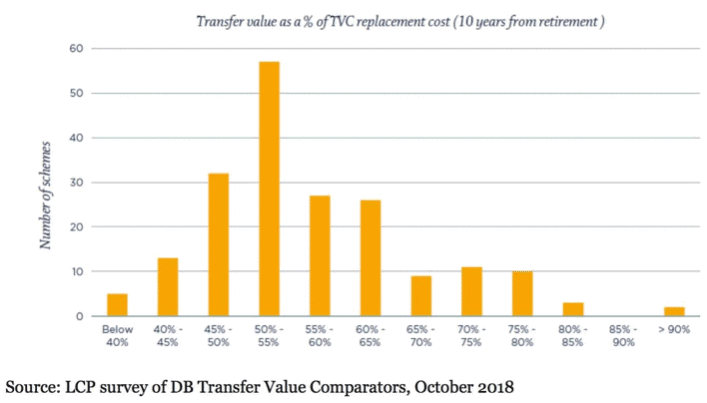

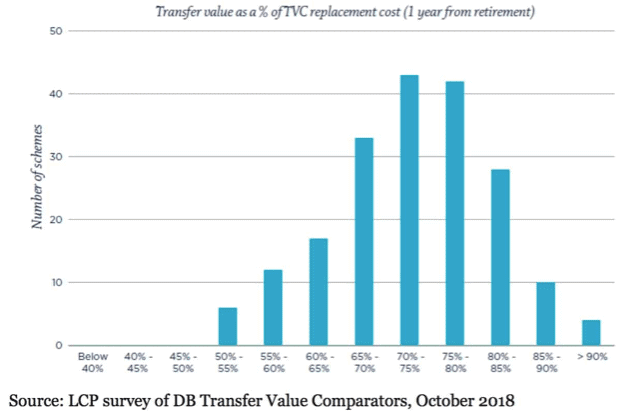

Plus, the benefits vs negatives around the differing levels of CETV multiples will change throughout your lifetime – age plays an enormous role in your CETV. A joint research paper by Royal London LCP suggested that the more generous CETV multiples are offered the closer you get to your scheme retirement age.

So, as well as asking yourself ‘should I transfer my final salary pension?’ you should also ask ‘is now the right time’?

Does CETV increase with age?

Largely, yes – however, that doesn’t make it a reliable means of making your final decision.

The below graph shows that, typically, the closer an individual gets to their retirement age, the higher their CETV will be.

Except… This doesn’t paint a full picture, does it? You cannot time the market. If transfer values tank – as they did so drastically in March 2020 – then age is no longer a guarantee. Such a dip could see values soar, or something else could step into the ring and make them shoot to the ground.

Values will also switch in response to factors such as interest rates and inflation. Our Pension Transfer Specialist Simon Garber says:

“Trying to time the market to get an increased transfer value is a risky game, I’ve seen people whose transfer values have gone up significantly, but I’ve also seen transfer values fall. If a Pension transfer makes sense, then it should be viewed as a long-term investment decision and shouldn’t ever be based on a short-term win. In short, the old adage usually holds true – time in the market is better than timing the market.

“Of course, it’s not going to be in everyone’s best interest to transfer their pension out of a Final Salary Scheme. If it’s not in your best interest to transfer, a rise in transfer value, even a generous one, probably won’t be enough to change this fact.”

Therefore, while age impacts your CETV, it is just one piece of a very large jigsaw.

Are CETV values increasing?

Over the past 12 months – since falling off of the cliff edge – we have seen a steady rise. While this has been promising, we are now experiencing another dip. While it is impossible to know for certain if we see a strong market recovery and rising interest rates post-covid we would expect transfer values to fall from the historic highs we saw in 2021. Since transfer values tend to have an inverse relationship with government investment bonds

CETV values 2020/2021.

2020 saw a typical ebb and flow of CETVs month to month – we saw gradual climbs and steady declines. That is until we hit March 2020, and the first lockdown. It was at this point that we were faced with a shockingly sharp decline.

Although, it didn’t take long to return to a more level playing field – again, with peaks and troughs – and a new record high in June 2020. XPS Pensions Group’s Transfer Value Index rose from £258,600 at the end of May to reach a record high of £260,800 in mid-June 2020. The number of Defined Benefit Scheme members opting to transfer out increased in June to 1.05% of eligible members. However, in reality, this still represents just over 10 in every 1,000 eligible members transferring each year.

Fast forward to 2021, and we are now finding ourselves in another considerable drop. In fact, February 2021 saw transfer values plunge to levels that haven’t been seen since pre-lockdown. This could, consequently, impact any alternate pensions that your transfer value could provide.

If you’re considering a pension transfer, It is vital that you discuss this with a pension transfer specialist. As a starting point, we have created a deferred final salary pension calculator. This calculator will give you a realistic high and low CETV estimate, based on current industry averages. It is intended to guide you through the initial steps; for a definitive value, you will need to request a CETV from your scheme directly.

Gilt yields and CETV

Gilts are British Government Bonds issued by HM Treasury. Essentially, this is how the UK government funds their borrowing. They pay a fixed amount of interest – over a set period of time – and you are guaranteed to get the face value back at the end of the time period.

However, the “face value” of the bond doesn’t necessarily reflect how much it is worth. That’s because they can be traded on the open market after they are purchased, which means their price can go down as well as up.

This matters when considering your CETV as the two are closely linked: as the gilt yields go down, transfer values go up. Gilt values tend to be high when interest rates are low (or likely to be lowered) because the rate of interest they pay will typically beat anything you would get in a savings account. As a result, they will be in higher demand. The opposite is also true – if interest rates rise Gilt values can sink.

Gilt Yields underpin both the overall “funding position” of a final salary scheme – the ratio of assets to liabilities – and the transfer values it offers to members.

Speaking to a Final Salary Pension Transfer specialist

If your Pension Transfer Value is over £30,000, you’ll need advice from a Final Salary Pension Transfer Specialist in order to move it.

A transfer specialist is there to show you whether or not a pension transfer is the right choice for you. They will do this by taking a holistic view of your:

- Current financial situation

- Future financial goals and retirement plans

- Family and dependents

- Experience of investing and your attitude towards risk

If you’d like to speak to a specialist, get in touch to arrange a free, no obligation introductory chat

{kind=link}